common strategy for Nigerian investors seeking a predictable and low-risk income stream.

Learn how FGN Savings Bonds work, their ₦5,000 entry point, quarterly interest payments, and why they are ideal for beginner investors in Nigeria.

This is indeed a common strategy for Nigerian investors seeking a predictable and low-risk income stream. Let's break down how this "salary" or "laddering" strategy works and provide you with a more accurate picture of the numbers.

Analyzing the "Salary" (Bond Laddering) Strategy.

1. The Mechanics (April Example)

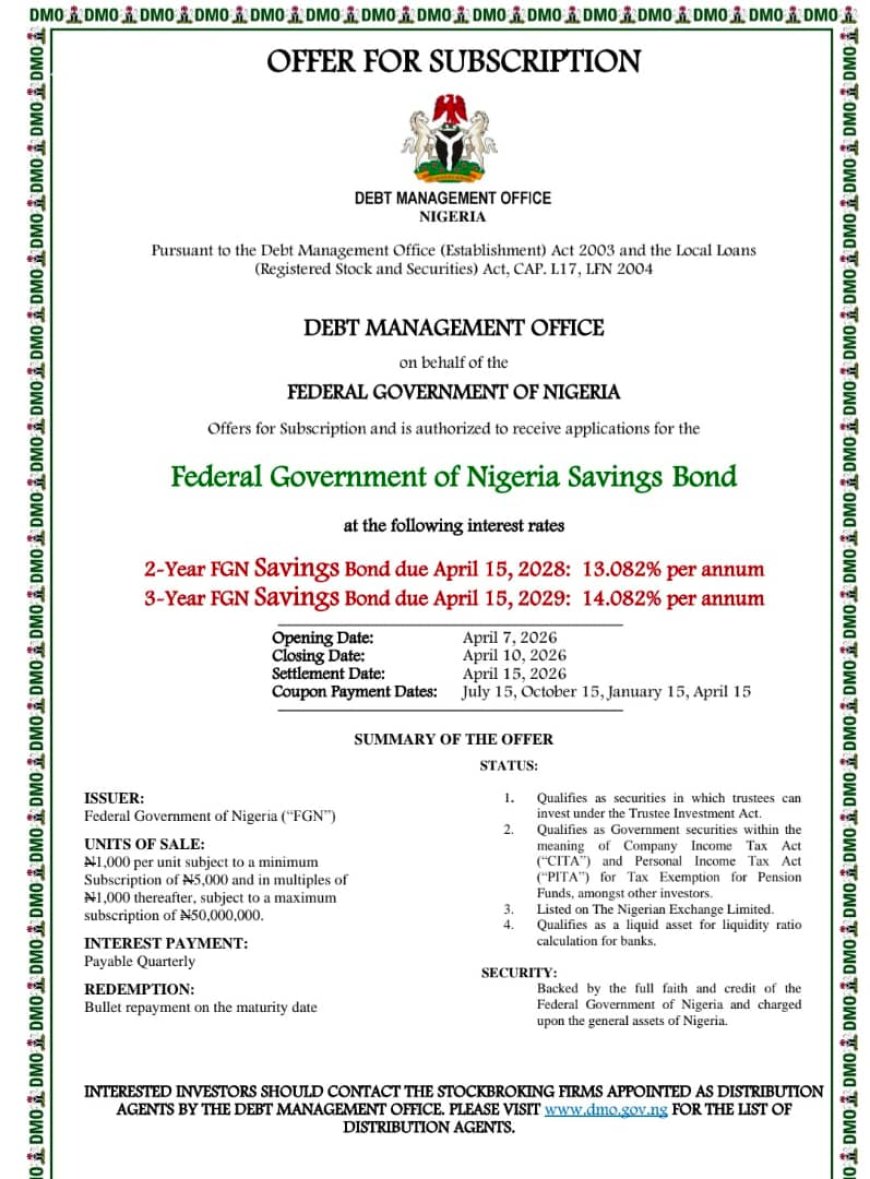

The figures you provided for April are very close to the standard FGN Savings Bond structure:

Principal Investment: ₦1,000,000

2-Year Rate: 13.082% per annum

3-Year Rate: 14.082% per annum

Frequency of Payment: Quarterly (every three months), not monthly. This is a critical distinction.

2. Correcting the Income Calculation

If you invest ₦1 million in the 3-year bond (14.082%):

Total Annual Interest: 14.082% of ₦1,000,000 = ₦140,820.

Quarterly Payment: ₦140,820 divided by 4 = ₦35,205 every three months.

Is it ₦11.7k/month?

Yes, but with a major catch. While ₦140,820 divided by 12 months is ₦11,735, you do not receive this money monthly. You receive the full ₦35,205 bulk sum every quarter (e.g., in January, April, July, and October).

To make this a true "monthly salary," you would have to manually budget that quarterly payment yourself, only spending ₦11,735 each month until the next payment arrives.

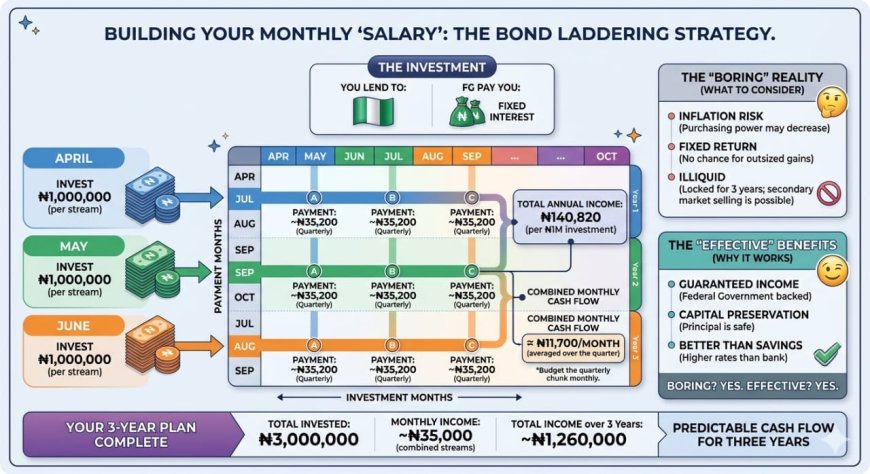

Building the 3-Year "Salary" (The April-June Ladder)

This is a smart approach called Bond Laddering. To create a true monthly income stream for three years using 3-year bonds, you would invest equal amounts in three consecutive months (April, May, and June).

Let’s assume you want an approximate "monthly salary" of ₦35,000 (close to the quarterly payment of one ₦1M investment):

Your Total Investment Required: ₦3 Million (₦1M in April, ₦1M in May, ₦1M in June).

How the Payment Schedule Would Look:

You now have 3 separate streams of quarterly income:

1. Stream A (April Invested): Pays you ₦35,205 in July, October, January, and April (for 3 years).

2. Stream B (May Invested): Pays you ₦35,205 in August, November, February, and May (for 3 years).

3. Stream C (June Invested): Pays you ₦35,205 in September, December, March, and June (for 3 years).

Your New Cash Flow Calendar:

April: Stream A pays (₦35,205)

May: Stream B pays (₦35,205)

June: Stream C pays (₦35,205)

July: Stream A pays (₦35,205)

...and so on.

By setting this up over three months, you create a schedule where one of your bond investments pays out every single month. You have successfully built a monthly "salary" for the next three years.

The "Boring But Effective" Analysis.

This strategy is highly effective for several reasons, perfectly fitting your description.

1. The Effective Part (The Pros)

Guaranteed Income: As long as the Federal Government of Nigeria exists and services its debt, you are guaranteed to receive your interest payments.

Capital Preservation: Your initial principal (the ₦3M) is protected and returned to you in full at the end of the 3-year term.

Superior to Savings Accounts: The interest rates (13% - 14%) are significantly higher than what you would get from a standard bank savings account.

Low Entry Barrier: You can start investing in FGN Savings Bonds with as little as ₦5,000.

2. The Boring Part (The Cons)

Inflation Risk (The Big Issue): Inflation in Nigeria is currently significantly higher than 14%. While your investment is "safe" and you are earning 14%, your purchasing power is actually decreasing because the cost of goods is rising faster than your investment is growing. This is the main downside of fixed-income investing in high-inflation environments.

Fixed Return: You know exactly what you will get. There is no opportunity to "hit it big" (like you might with a successful stock investment) during the 3-year term.

Illiquidity: Your money is locked away. While you can sell bonds before maturity on the secondary market, it can be a slow process, and you might have to sell at a loss if interest rates have risen since you invested.

Final Take

You are correct: this strategy is "boring but effective." It is an excellent foundation for any investment portfolio, particularly for capital preservation and creating a predictable cash flow. For a risk-averse Nigerian investor or someone planning for a fixed future expense, it's a solid and powerful tool.