Systemizing Wealth Building

Wealth isn't built by luck or willpower; it's built by systems. This comprehensive guide shows Nigerian investors how to design automated, repeatable financial processes that grow wealth in the background of everyday life. From Pay-Yourself-First to dollar-cost averaging, compound interest to multiple income streams, here's your complete blueprint.

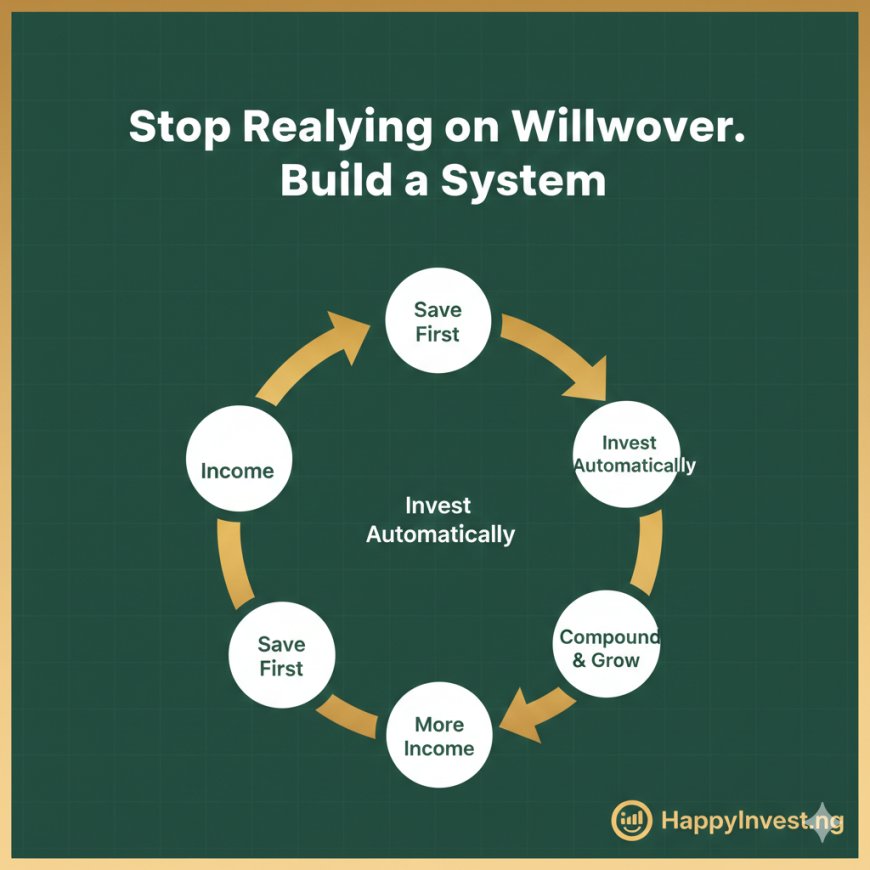

Wealth is not built by luck, income, or occasional good decisions. It is built by systems, repeatable, automatic processes that work relentlessly in the background, whether you're paying attention or not.

Think about the wealthiest people you know of. What's the first thing you might assume about them? That they're smarter than average? That they had a lucky break? That they earn extraordinary incomes?

Sometimes those things are true. But more often than not, the defining characteristic of people who build lasting, generational wealth is not intelligence, luck, or even income. It is discipline, and more specifically, it is the systems they put in place that made discipline automatic.

Because here is the uncomfortable truth about human nature: we are not wired for long-term thinking. We prefer immediate gratification over delayed rewards. We forget to invest when life gets busy. We spend impulsively when we're stressed or celebrating. We make emotional financial decisions when markets are volatile. We are, in short, our own worst financial enemies.

The solution is not to try harder or want it more. The solution is to build systems that remove the need for willpower altogether, systems that automate the right behaviours, protect you from your worst impulses, and compound quietly in the background while you live your life.

This is what we mean by systemizing wealth building. And in this article, we'll show you exactly how to do it with specific, practical strategies tailored for the Nigerian investor.

1. Why Systems Beat Willpower Every Time

Willpower is a finite resource. Research by psychologist Roy Baumeister showed that self-control draws on a limited mental energy, and the more decisions you make in a day, the more depleted your willpower becomes. This is why the same person who sticks perfectly to a budget in the morning will impulse-buy something expensive in the evening after a long, draining day.

Applied to personal finance, this means that any wealth-building strategy that depends on you constantly choosing the right thing, choosing to save instead of spend, choosing to invest instead of defer, choosing to stay the course instead of panic-selling, is fundamentally fragile. Life will eventually overwhelm your willpower, and the system will break down.

Systems, on the other hand, are not subject to willpower depletion. A standing order that automatically moves ₦50,000 from your current account to your investment account on the 1st of every month does not care whether you had a hard week or whether there's a flash sale at your favourite mall. It just executes.

|

The most successful wealth builders don't rely on motivation; they design environments and processes where the right financial behaviour happens automatically, and where the wrong behaviour requires active effort to execute. |

This is the foundational insight behind systemizing wealth building: the goal is to make good financial decisions the path of least resistance, and bad financial decisions the path of most resistance.

2. The Master System: Pay Yourself First

If you were to implement only one wealth-building system for the rest of your life, it should be this: Pay Yourself First.

Pay Yourself First flips this model entirely: earn income → immediately transfer your savings/investment amount → live on the rest. Your wealth-building contribution is treated not as an afterthought but as the first and most non-negotiable bill you pay — to your future self.

|

How it works in Nigeria: On your salary payment date, set up an automatic transfer to a dedicated savings or investment account before you do anything else, before paying rent, before DSTV, before airtime. Treat it like a mandatory deduction, just like PAYE tax. What you never see, you never miss. |

What Percentage Should You Pay Yourself?

A common starting framework is the 50/30/20 rule: 50% of net income goes to needs (rent, food, utilities, transport), 30% to wants (entertainment, dining out, shopping), and 20% to savings and investments. In the Nigerian context, where the cost of living pressures are high, even starting at 10% is valuable, with a plan to increase the percentage as your income grows.

3. The Architecture of a Wealth-Building System

A complete wealth-building system is not a single action but a set of interconnected processes, each serving a specific role. Think of it as a financial assembly line: money enters at one end, flows through a structured series of steps, and emerges at the other end as growing, compounding wealth.

Here are the core components:

|

01 |

Income Optimisation Maximize what flows into your system. This means negotiating your salary, developing multiple income streams, upgrading your skills to command higher pay, and monetizing underused assets. No system can compensate for insufficient input. |

|

02 |

Automated Saving Set up standing orders that automatically move a fixed amount to savings/investment accounts on payday. Remove human decision-making from this step entirely. Use dedicated accounts separate from your spending account. |

|

03 |

Structured Spending Create a budget — but make it automated. Use envelope budgeting or dedicated accounts for different spending categories. When the month's food budget runs out, you stop spending on food. No exceptions, no willpower required. |

|

04 |

Debt Elimination Protocol If you carry high-interest debt (personal loans, credit card debt), your system must include a debt destruction plan. High-interest debt is a negative compounding engine working against you. Eliminate it systematically before accelerating investments. |

|

05 |

Tiered Investment Deployment Saved money must be deployed into assets that grow. Your system should define clear tiers: emergency fund first, then tax-advantaged retirement savings, then broader investment portfolio. Each tier has a target balance that triggers movement to the next. |

|

06 |

Automated Portfolio Rebalancing Set a calendar reminder or use platforms that auto-rebalance to review and restore your target asset allocation annually. This enforces the discipline of buying low and selling high without emotional interference. |

|

07 |

Protection Layer Adequate life, health, and income protection insurance ensures that a single catastrophic event — illness, accident, death — cannot destroy the wealth your system is building. Insurance is not a wealth builder, but it is a wealth preserver. |

|

08 |

Annual System Review Once a year, review every component of your system. Are the amounts appropriate given income changes? Are the investment accounts performing? Is your asset allocation still aligned with your goals and timeline? Adjust, then automate again. |

4. The Compound Interest Engine: Why Time Is Your Most Valuable Asset

No article on systemizing wealth would be complete without a deep look at the most powerful force in personal finance: compound interest. Albert Einstein reportedly called it the eighth wonder of the world, and while the attribution may be apocryphal, the sentiment is accurate.

Compounding means earning returns not just on your original investment, but on all the returns your investment has previously generated. It's interest on interest, growth on growth and over time, it produces results that seem almost impossible.

To understand why this makes starting early so critical, consider two Nigerian investors:

▸ Investor A (Amaka) starts investing ₦50,000 per month at age 25 and stops at age 35, investing for just 10 years, then leaves the money untouched until retirement at 60.

▸ Investor B (Bello) waits until age 35 to start, then invests ₦50,000 per month all the way to age 60, investing for 25 consecutive years.

Who ends up wealthier at 60? Amaka by a significant margin despite investing for far fewer years and putting in far less money. This is the power of time in a compounding system, and it is why the most important financial decision for a young Nigerian is not which stocks to pick but simply to start investing now, today, whatever amount is possible.

The Power of Consistent Monthly Investment at 12% Annual Return

|

Years Investing |

Monthly Investment |

Total Invested |

Portfolio Value (12% p.a.) |

|

10 years |

₦50,000 |

₦6,000,000 |

₦11,500,000 |

|

20 years |

₦50,000 |

₦12,000,000 |

₦49,900,000 |

|

30 years |

₦50,000 |

₦18,000,000 |

₦176,000,000 |

|

35 years |

₦50,000 |

₦21,000,000 |

₦324,000,000 |

Note: Assumes 12% annual return (approximate long-term NGX average). For illustration purposes. Actual returns will vary.

|

The numbers above are not magic; they are mathematics. ₦50,000/month for 35 years at 12% p.a. produces over ₦324 million. The system does the work. Your only job is to start the system and not stop it. |

5. Automating Your Investment Contributions in Nigeria

The good news for Nigerian investors is that the financial infrastructure for automating wealth building has improved dramatically in recent years. Here's how to set up automation across different investment vehicles:

Money Market & Mutual Funds

Platforms like Cowrywise, Piggyvest, and Risevest all offer automated recurring investment features. You can set a fixed amount to be automatically debited from your bank account weekly or monthly and invested into money market funds, dollar funds, or curated investment portfolios. This is the simplest entry point for automated investing in Nigeria.

NGX Stock Market

Several Nigerian stockbrokers and investment platforms, including Bamboo (for US stocks) and Trove, offer recurring investment features. You can set up automatic purchases of ETFs or specific stocks on a schedule, implementing a strategy called dollar-cost averaging (DCA) without any manual effort each month.

FGN Bonds & Treasury Bills

While these don't yet have fully automated purchase systems in Nigeria, you can create a system by setting a calendar reminder to participate in each auction through the Debt Management Office (DMO) portal or via your bank. Better yet, reinvestment of matured T-Bills can often be arranged with your bank automatically.

Pension Contributions (RSA)

If you're employed in Nigeria, your Retirement Savings Account (RSA) under the Contributory Pension Scheme is already an automated wealth-building system — 8% of your monthly salary is automatically deducted and invested by your PFA (Pension Fund Administrator). Voluntary Additional Voluntary Contributions (AVCs) can boost this further and offer tax advantages.

Real Estate Through REITs

Instead of saving sporadically for a lump-sum property purchase, you can invest small, regular amounts into UPDC REIT or similar real estate investment trusts listed on the NGX, building exposure to real estate systematically over time without the need for a large upfront capital.

|

System Tip: Create a dedicated 'investment account' separate from your spending account and ideally at a different bank that exists solely to receive your automated savings and deploy them into investments. The psychological barrier of logging into a separate institution adds friction to impulsive withdrawals. |

6. Dollar-Cost Averaging: The System Within the System

One of the most powerful and simple wealth-building systems is dollar-cost averaging (DCA) — or in our context, naira-cost averaging. The concept is straightforward: instead of trying to time the market and invest a lump sum at the 'perfect moment,' you invest a fixed amount at regular intervals regardless of market conditions.

When prices are high, your fixed investment buys fewer units. When prices are low, the same investment buys more units. Over time, this automatically results in a lower average cost per unit than if you'd tried to time the market — and it removes the emotional agony of trying to decide when to invest.

|

Example: You invest ₦30,000 in NGX ETFs every month for 12 months. In January, units cost ₦150. You buy 200 units. In March, during a market dip, units cost ₦100; you buy 300 units automatically. By year-end, you've accumulated more units at a lower average cost than if you'd invested the full ₦360,000 in January. The system exploits market volatility rather than being destroyed by it. |

DCA is not the highest-return strategy in all scenarios. If markets go straight up, a lump-sum investment at the start would outperform. But it is the strategy that works consistently for most people across all market conditions, while also managing behavioural risk. It is, in other words, a system designed for the way humans actually behave rather than the way financial models assume they do.

7. Building an Emergency Fund: The System's Foundation

Every wealth-building system must be built on a solid foundation, and that foundation is an emergency fund. This is 3–6 months of essential living expenses, held in a liquid, accessible account (not invested in volatile assets), available at any time without penalty.

Without an emergency fund, any unexpected expense, a medical bill, a car repair, or job loss forces you to raid your investment portfolio, disrupting compounding and potentially triggering tax consequences or penalties. With an emergency fund, unexpected expenses are absorbed by the buffer, and your wealth-building system continues uninterrupted.

For a Nigerian household with monthly essential expenses of ₦150,000, an appropriate emergency fund is ₦450,000 to ₦900,000 held in a high-yield savings account or money market fund where it earns a return while remaining accessible.

|

Building your emergency fund IS your first investment. Before contributing to stock market investments, before buying bonds, before anything else, fund your emergency account to 3 months of expenses. Only then activate the rest of your wealth-building system. |

8. Income Diversification: Building Multiple Input Streams

The most robust wealth-building systems are not dependent on a single source of income. Just as a well-allocated investment portfolio is not dependent on a single asset class, a well-designed financial life is not dependent on a single income stream.

Building additional income streams does not necessarily mean working multiple jobs until you're exhausted. It means systematically developing assets, both financial and intellectual, that generate income independently. For a Nigerian professional, this might include:

▸ Dividend income from NGX-listed stocks (Zenith Bank, Stanbic IBTC, and others have historically paid consistent dividends)

▸ Rental income from residential or commercial property

▸ Interest income from bonds, treasury bills, and money market funds

▸ Freelance or consulting income from your professional expertise

▸ Digital income streams: online courses, e-books, content creation, affiliate marketing

▸ Business equity: ownership stakes in small businesses or startups

The system here is intentional diversification over time — not trying to build all of these at once, but adding one new income stream every 1–2 years as your skills, capital, and capacity allow. Each new stream increases your system's resilience and accelerates the rate at which you can invest.

|

The goal of multiple income streams is not just more money — it is security. When one stream slows or stops (as happens in every economy), the others sustain your wealth-building contributions. The system keeps running even when one engine sputters. |

9. The Psychological Infrastructure of a Wealth System

Systems are not just technical — they also have a psychological dimension. The most brilliantly designed financial system will fail if the person operating it doesn't have the right mental frameworks. Here are the mindset systems that support the technical ones:

Define Your 'Why' in Concrete Numbers

Vague goals produce vague commitment. 'I want to be wealthy someday' is not a system — it's a wish. 'I want to have ₦100 million in investments by age 50, generating ₦1 million per month in passive income' is a target you can reverse-engineer into a monthly savings rate and investment return requirement. Specificity creates urgency and direction.

Automate, Then Ignore

One of the psychological risks of active investing is constantly checking your portfolio's performance, which leads to emotional reactions to short-term volatility. Once you have set up your automated contributions and asset allocation, the discipline is not look too often. Checking your portfolio daily is a recipe for anxiety and bad decisions. Monthly is sufficient for most investors; quarterly is fine for long-term portfolios.

Celebrate Process, Not Just Outcomes

Wealth building is a long game measured in decades. If you only celebrate outcomes (hitting a net worth target), you will spend most of your journey feeling frustrated. Build the habit of celebrating process adherence, making your automated investment this month, resisting an impulsive large purchase, and increasing your contribution percentage after a raise. These process wins are the real leading indicators of financial success.

Design Your Environment for Success

Remove friction from good financial behaviour and add friction to bad financial behaviour. Unsubscribe from retailer emails. Delete shopping apps from your phone. Use a separate bank for investments that require you to physically walk in to withdraw (or at least transfer with a 24-hour delay). Make it easy to save and hard to spend impulsively.

Your Wealth-Building System Blueprint

Here is a practical, step-by-step blueprint to implement your system today:

▸ Calculate your monthly net income and essential expenses to determine how much you can allocate to wealth building — start with at least 10%, ideally 20%.

▸ Open a dedicated investment account at a different institution from your spending account.

▸ Set up a standing order on your salary date to automatically transfer your wealth-building amount to this account.

▸ If you don't yet have a 3-month emergency fund, direct these contributions there first until the fund is complete.

▸ Once your emergency fund is complete, activate your investment contributions: start with money market funds or mutual funds for simplicity, then expand into bonds, NGX stocks/ETFs, and eventually global stocks as your confidence and capital grow.

▸ Set up a recurring investment schedule (monthly is ideal) on your chosen investment platform Cowrywise, Bamboo, Trove, or through your stockbroker.

▸ Set a calendar reminder every January for your annual system review: increase contribution amounts (especially after raises), rebalance your portfolio, review your insurance coverage, and set new wealth targets.

▸ Never turn off the system. Market downturns, salary cuts, and unexpected expenses will tempt you to pause contributions. Resist this temptation — market downturns are when your automated purchases of undervalued assets are most valuable.

Final Thoughts: The System Is the Strategy

We live in a culture that celebrates dramatic financial wins: the startup that became a unicorn, the investor who bought Bitcoin at $500, the trader who turned ₦100,000 into ₦10 million in a year. These stories are real, but they are also rare, unreplicable, and often come with untold stories of catastrophic losses along the way.

The less exciting but far more reliable path to wealth is the one described in this article: a disciplined, automated, patient system that works quietly in the background of your life, compounding your contributions into life-changing wealth over 20, 30, or 40 years.

The Nigerian economic environment, with its inflation pressures, currency volatility, and income uncertainty, makes systematic wealth building not just a good idea but an urgent necessity. The cost of not having a system is not stagnation; it is slow financial erosion, as inflation silently destroys the purchasing power of money that isn't growing.

Build your system today. Automate it ruthlessly. Then be patient enough to let time and compounding do what they do best.

At HappyInvest.ng, we exist to help you build that system with the knowledge, tools, and community you need to achieve genuine financial freedom in Nigeria and beyond.

The wealthiest version of your future self is not waiting on a lucky break. They're waiting on you to build the system.