FGN Savings Bonds: A Safe Investment Option for Small Investors in Nigeria

Discover FGN Savings Bonds in Nigeria. Learn about the ₦5,000 minimum investment, quarterly coupons, and how they compare to traditional bonds.

For many Nigerians, investing used to feel like something only “big money” could access.

But that changed with the introduction of FGN Savings Bonds, a simple, low-risk way for everyday people to invest in government-backed securities.

If you want:

-

Safety

-

Predictable income

-

A low entry point

Then, FGN Savings Bonds are worth understanding.

What Are FGN Savings Bonds? (Simple Definition)

FGN Savings Bonds are government-backed investment instruments that allow individuals to lend money to the Federal Government of Nigeria and earn interest.

In simple terms:

You lend money to the government, and they pay you interest on a regular basis.

The Debt Management Office of Nigeria issues them on behalf of the Federal Government.

Why They Were Introduced

FGN Savings Bonds were designed to:

-

Encourage a savings culture

-

Give small investors access to government securities

-

Provide a safe investment option

Key Feature: The ₦5,000 Entry Point

One of the biggest advantages is affordability.

Minimum Investment

-

₦5,000

Additional Investments

-

In multiples of ₦1,000

Why This Matters

Traditional government bonds often require:

-

Hundreds of thousands or millions of naira

But FGN Savings Bonds:

-

Allow almost anyone to start

This makes them ideal for beginners and small investors.

Quarterly Coupon Structure (How You Earn Money)

FGN Savings Bonds pay interest through what is called a coupon.

How It Works

-

You invest a fixed amount

-

The government pays you interest every 3 months (quarterly)

-

At maturity, your original money is returned

Example

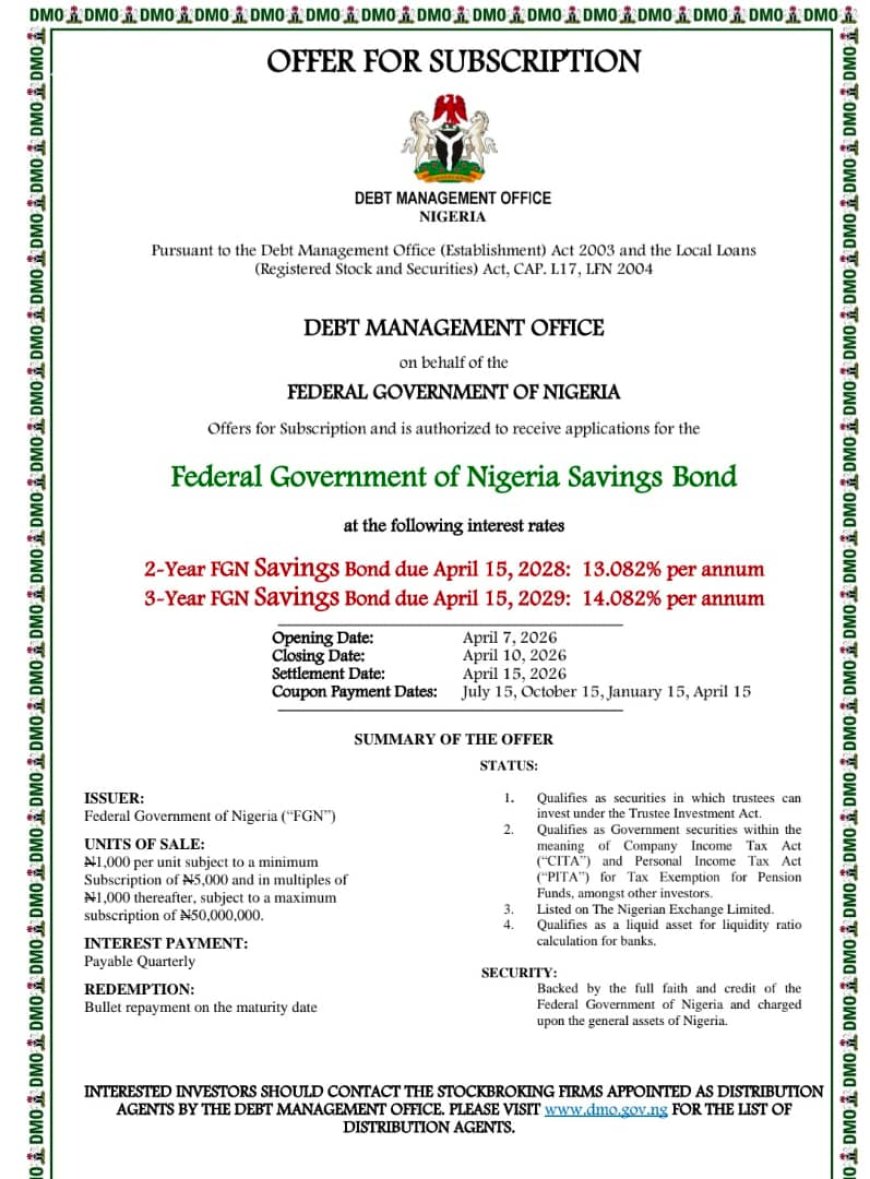

April rates: 13.082% (2yrs) | 14.082% (3yrs)

₦1M ≈ ₦11.7k/month.

Invest April, May, June = 3 separate streams.

You’ve built a monthly “salary” for 3 years.

If:

-

You invest ₦100,000

-

The annual interest rate is 12%

Then:

-

You earn ₦12,000 per year

-

Paid as ₦3,000 every 3 months

Why This Is Attractive

-

Regular income

-

Predictable returns

-

No need to wait until maturity

Availability: When Can You Buy FGN Savings Bonds?

FGN Savings Bonds are typically:

-

Offered monthly

-

Open for subscription for a few days (usually early in the month)

You can invest during these offer windows.

How to Buy FGN Savings Bonds

You can invest through:

-

Licensed stockbrokers (Invest Naija, i-invest, Afrinvestor 2.0, Bamboo, etc)

-

Investment platforms connected to the Nigerian Exchange Group

Basic Steps

-

Open a brokerage account

-

Fund your account

-

Subscribe during the offer period

-

Receive quarterly interest payments

FGN Savings Bonds vs Traditional FGN Bonds

1. Minimum Investment

| Feature | FGN Savings Bonds | Traditional FGN Bonds |

|---|---|---|

| Minimum | ₦5,000 | Typically ₦50,000 – ₦100,000+ (or more via auctions) |

2. Accessibility

| Feature | FGN Savings Bonds | Traditional Bonds |

|---|---|---|

| Target | Retail investors | Institutional & high-net-worth investors |

3. Purchase Method

| Feature | FGN Savings Bonds | Traditional Bonds |

|---|---|---|

| Access | Simple via brokers | Auction system (more complex) |

4. Income Structure

Both:

-

Pay fixed interest (coupons)

-

Offer predictable returns

But FGN Savings Bonds are:

-

More beginner-friendly

Who Are FGN Savings Bonds For?

1. Beginners

Easy to understand and start.

2. Low-Risk Investors

Backed by the government.

3. Income Seekers

Quarterly payments provide a steady cash flow.

4. Long-Term Savers

Helps build disciplined investing habits.

Advantages of FGN Savings Bonds

1. Safety

Backed by the Federal Government.

2. Low Entry Barrier

Start with just ₦5,000.

3. Regular Income

Quarterly interest payments.

4. Predictability

Fixed returns reduce uncertainty.

5. Accessibility

Easy to buy through brokers.

Disadvantages to Consider

1. Lower Returns Compared to Stocks

Safer, but not high-growth.

2. Inflation Risk

Returns may not always beat inflation.

3. Limited Liquidity

You may need to wait or sell in the secondary market.

Simple Strategy for Beginners

Step 1

Start with ₦5,000 – ₦50,000

Step 2

Reinvest your quarterly interest

Step 3

Combine with:

-

Treasury bills

-

Money market funds

Step 4

Gradually add higher-growth assets like stocks

Real-Life Example

Person A

-

Keeps money idle

-

Earns little or nothing

Person B

-

Invests in FGN Savings Bonds

-

Earns a steady quarterly income

Over time:

-

Person A loses value to inflation

-

Person B builds disciplined savings and income

Small Steps, Strong Foundation

FGN Savings Bonds prove that:

You don’t need a lot of money to start investing.

With:

-

Low entry

-

Government backing

-

Regular income

They are one of the safest starting points for Nigerian investors.

Because in the end:

Building wealth is not about starting big; it is about starting right and staying consistent.