The Smart 20-Year Wealth Strategy Most Young Nigerians Are Ignoring

Discover how to design a 20-year wealth plan in Nigeria using an all-weather portfolio strategy for growth, stability, and financial independence.

Ray Dalio built a strategy that survives every economic season, inflation, recession, boom, and deflation. Here is how young Nigerians, aged 18–35, can adapt it to the realities of the NGX, naira volatility, FGN bonds, and gold and use it to build life-changing wealth by 2045.

- Who Ray Dalio is and why his strategy matters for Nigeria

- The philosophy: four economic seasons, one portfolio

- The original All-Weather allocation

- Why Nigeria needs its own adaptation

- The Nigerian All-Weather Allocation

- The instruments: what to buy in Nigeria for each layer

- The 20-Year Wealth Timeline: four phases

- Projected wealth accumulation scenarios

- Annual rebalancing and portfolio maintenance

- Common mistakes that break the strategy

11. Your action plan starts this month

1. Who Ray Dalio Is and Why His Strategy Matters for Nigeria

Ray Dalio founded Bridgewater Associates in his Manhattan apartment in 1975. Over five decades, he built it into the world's largest hedge fund, managing over $100 billion in assets, and generated more net investment profits than any other fund in history. His investment philosophy, refined through every major economic crisis from the 1970s stagflation to the 2008 global financial collapse, centres on one insight that sounds deceptively simple: nobody can consistently predict the future direction of markets.

Instead of fighting that uncertainty, Dalio's approach harnesses it. He created a portfolio structure designed not to win in any specific economic scenario, but to survive and grow through all of them, rising growth, falling growth, rising inflation, and falling inflation. He called it the All-Weather Portfolio, and its core principle, risk parity across economic environments, is as relevant in Lagos and Abuja as it is in New York.

For young Nigerians aged 18–35 in 2026, the All-Weather philosophy is particularly powerful because Nigeria is, by definition, a high-volatility economic environment. Oil price crashes, naira devaluation, inflation spikes, political transitions, and banking sector crises have hit Nigerian investors without warning across every decade since independence. The All-Weather strategy was specifically built for this kind of world.

The core insight: The All-Weather Portfolio does not try to predict which economic season comes next. It owns assets that do well in every season, balanced so that no single environment can devastate the portfolio. For Nigerians dealing with unpredictable naira movements and commodity shocks, this is not a luxury philosophy; it is essential risk management.

2. The Philosophy: Four Economic Seasons, One Portfolio

Dalio identified that all economic environments can be mapped across two dimensions: growth (rising or falling) and inflation (rising or falling). This creates four possible economic "seasons." The revolutionary insight is that different asset classes perform well in different seasons, and you cannot know which season comes next. The solution is to hold something that works for each.

"I can keep the same return as any one of those investments with up to an 80% reduction in risk if I have 10 to 15 good uncorrelated return streams, risk-balanced across them." Ray Dalio, Principles (2017)

3. The Original All-Weather Allocation

Dalio's widely cited public approximation of the All-Weather Portfolio, designed for US institutional investors, allocates capital as follows:

Over the past 30 years, this allocation has delivered a 7.33% compound annual return with a maximum drawdown of just −20.58% compared to 50%+ for an all-equity portfolio during the 2008 crisis. In 65% of all months since 2006, the portfolio was positive. It doubles an investment approximately every 10 years.

4. Why Nigeria Needs Its Own Adaptation

The original All-Weather Portfolio was designed for US investors in US dollars. Applying it directly to a Nigerian context creates several mismatches that must be corrected:

Currency risk: US Treasury bonds perform in USD. A Nigerian holding USD bonds benefits when the naira weakens, but if the naira strengthens (as it briefly did in late 2024), the naira value of those bonds falls. The portfolio must acknowledge that Nigerian investors live and spend in naira.

Naira inflation is structurally higher: Nigerian inflation has averaged 12–25% over the past decade, dramatically higher than US inflation. Fixed-income instruments that protect US investors may not even keep pace with the purchasing power of the naira. The Nigerian portfolio needs higher-yielding naira instruments plus genuine FX hedging.

The NGX is an emerging market with different cycles: Nigerian equities sometimes move completely independently of global markets. The NGX returned +50% in 2020 when global markets were crashing due to COVID. It fell sharply in 2015–2016 when US markets were recovering. Nigerian equities deserve specific allocation as a distinct asset class, not a proxy for global stocks.

Limited bond market depth: The Nigerian bond market, while growing significantly, does not yet have the same long-duration instruments available in the US. FGN bonds go up to 30 years, but liquidity is concentrated in shorter maturities. The bond allocation must be adapted accordingly.

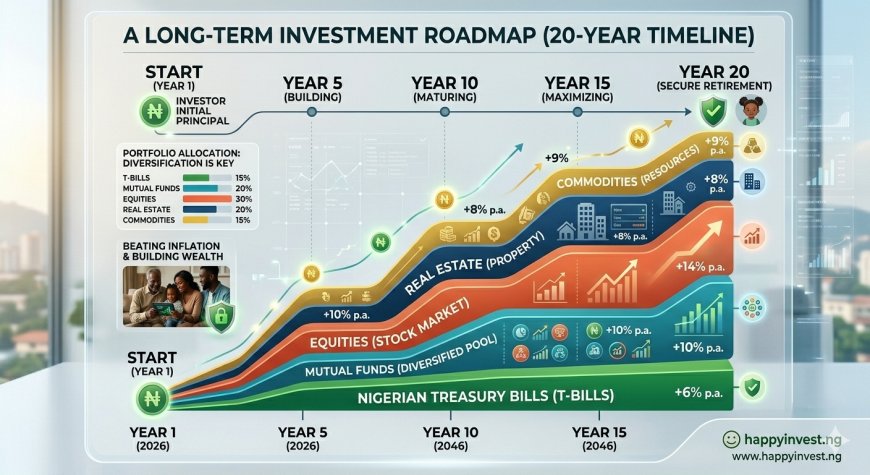

5. The Nigerian All-Weather Allocation

The following adaptation maintains the risk-parity philosophy of the original while replacing US instruments with their Nigerian and Nigeria-accessible equivalents. It is designed for a young Nigerian investor aged 18–35 with a 20-year horizon.

Key adaptation: The original 7.5% commodities allocation is split into 10% gold (via NewGold ETF), and the commodities portion is replaced by a 15% USD dollar asset allocation. This directly addresses Nigeria's unique currency risk, the single greatest threat to long-term Nigerian wealth accumulation that the original portfolio does not protect against.

6. The Instruments: What to Buy in Nigeria for Each Layer

Starting capital requirement: This portfolio can be started with as little as ₦10,000 per layer (₦50,000 total across five layers). The minimum investment on Cowrywise is ₦5,000. Meristem starts from ₦5,000. Risevest from $10. There is no wealth threshold; there is only consistency over time.

7. The 20-Year Wealth Timeline: Four Phases

8. Projected Wealth Accumulation Scenarios

The following projections assume an average blended portfolio return of 18% annually in naira terms (conservative for Nigeria, given current yields) on a consistent monthly investment. This is conservative relative to recent actual performance but accounts for future economic uncertainty.

Disclaimer: These projections are illustrative only, based on a constant 18% annual blended return in naira terms. Actual returns will vary significantly year to year. The All-Weather strategy reduces volatility but does not eliminate it. Past performance of any asset class does not guarantee future results. These figures have not been adjusted for inflation.

9. Annual Rebalancing and Portfolio Maintenance

Rebalancing is what keeps the All-Weather strategy working over 20 years. Without it, strong performers naturally grow to dominate the portfolio, recreating the concentration risk the strategy was designed to eliminate. Here is the annual maintenance protocol:

1. Review current allocation percentages (January, every year)

Calculate the current value of each layer as a percentage of the total portfolio. If any layer has drifted more than 5% from its target, it needs rebalancing. Equities in a strong year may grow from 30% to 38%; that extra 8% must be trimmed and redistributed.

2. Sell overweight positions, buy underweight positions

Trim whatever has grown disproportionately. This systematically enforces buy-low-sell-high discipline without requiring any market prediction. In the 2024 NGX rally, your equity layer grew large, rebalancing locked-in gains and redeploying them into bonds and money market at their temporarily lower levels.

3. Reinvest all income received during the year

Record every dividend payment, bond coupon, and money market distribution received. Reinvest all of it into your underweight layers. This simultaneously accelerates compounding and rebalances the portfolio toward its targets.

4. Review and increase monthly contributions

Every January, assess whether your monthly contribution amount should increase. If your income has grown by 15%, your contributions should also grow ideally at the same rate. The portfolio allocation percentages stay constant; the naira amounts increase.

5. Update USD allocation for naira movements

The dollar layer is specifically designed to protect against naira devaluation. If the naira has strengthened significantly, your USD layer may be underweight in naira terms, so top it up. If the naira has weakened dramatically, your USD assets are now worth more in naira; the layer may be overweight and should be trimmed.

6. Keep investment records for tax purposes

Mutual fund gains are currently tax-free in Nigeria. Stock dividends are subject to withholding tax (currently 10%), which is deducted at source. Bond coupon income is also subject to withholding tax. Keep records of all transactions, distributions, and deductions for your own financial clarity and any future regulatory changes.

10. Common Mistakes That Break the Strategy

Abandoning the strategy during a bear market

The All-Weather Portfolio will underperform a pure equity portfolio during strong bull markets. In 2024–2025, when the NGX was up 38–51%, your All-Weather portfolio returned significantly less because 70% of it was in bonds, money market, gold, and USD assets. This is working as intended. The temptation to abandon the strategy and chase equities during bull markets is the single biggest threat to the long-term plan.

Withdrawing returns instead of reinvesting them

In years 1 through 10, every single naira of dividends, coupons, and interest must be reinvested. Spending returns early is like pulling bricks from the foundation of a building under construction. The compounding mathematics only deliver their extraordinary long-term outcomes if the base keeps growing.

Ignoring the dollar layer

Many young Nigerians find the complexity of dollar investing daunting and simply skip the USD layer. This is a critical error. Nigeria's history of naira devaluation — from ₦22/$1 in 2000 to over ₦1,500/$1 today means that naira-only wealth is vulnerable in a way that permanently impairs purchasing power. The 15% USD layer is the portfolio's structural insurance against this.

Overcomplicating the instrument selection

You do not need 20 different stocks and 10 different mutual funds. A clean Nigerian All-Weather Portfolio can be built with just five instruments: Vetiva Griffin 30 ETF (equities), Vetiva S&P Nigeria Sovereign Bond ETF (long bonds), Cowrywise ARM Money Market Fund (T-bills/money market), NewGold ETF (gold), Risevest Fixed Income (USD). Five instruments, five layers, rebalanced once annually. The simplest system that you actually maintain is far more valuable than a complex one that overwhelms you into inaction.

11. Your Action Plan Start This Month

W1. Open accounts on Cowrywise and Risevest

Both take under 30 minutes each. Cowrywise covers your money market (naira) layer. Risevest covers your USD layer. Both are SEC-regulated. Minimum investments start at ₦100 and $10, respectively.

W2. Open a stockbroking account (Meristem or CSL)

This gives you access to the NGX: equities, ETFs (Vetiva Griffin 30, NewGold ETF, SIAML Pension ETF 40), and bonds. Required for the equity and gold layers. Takes 1–3 business days to activate after KYC.

W3. Make your first contributions to all five layers

Even ₦10,000 per layer (₦50,000 total) activates the system. The amount matters less than the act of starting all five layers simultaneously. Each layer is now live and compounding.

W4. Set up monthly auto-debits for every layer

Standing orders execute automatically on payday. Your All-Weather portfolio contributions should require zero willpower after the first setup. Remove human emotion from the monthly investment decision entirely.

M2. Register for e-dividend on all NGX holdings

Ensure all dividend payments from NGX stocks and ETFs go directly to your bank account and then immediately into a reinvestment order. Unclaimed dividends are one of the most common ways Nigerian investors lose returns they have already earned.

Y1. Schedule your first annual rebalancing (January 2027)

Block a half-day in your calendar. Review all five layers. Trim overweight. Buy underweight. Reinvest all income received. Increase monthly contributions if income has grown. Record everything. Repeat every January for 20 years.

The Compound Truth About 20-Year Wealth

The All-Weather Portfolio will never make you rich quickly. That is not what it is designed to do. It is designed to make you rich inevitably through a disciplined, systematic process of diversified accumulation that survives every economic storm Nigeria has ever produced and every one it will produce over the next two decades.

In a country where 70% of Nigerians die without a Will and most investors have no systematic long-term plan, committing to a 20-year All-Weather strategy places you in a genuinely rare category. The people who build generational wealth in Nigeria over the next 20 years will not be those who picked the best stock in 2026. They will be the ones who built a system in 2026 and did not break it.

The Nigerian economic environment, with its inflation, volatility, currency pressures, and political uncertainty, is not a reason to avoid investing. It is the reason this strategy exists. Build your All-Weather portfolio today. Rebalance it every January. Reinvest every naira of return for at least 10 years. And in 2045, look back at the decision you made this month.

Your single action today: Download Cowrywise. Invest ₦10,000 in the ARM Money Market Fund. You have started Layer 3 of your All-Weather Portfolio. Everything else is built one layer at a time from there.

Disclaimer: This article is for educational purposes only. It does not constitute personalized financial or investment advice. All investments carry risk, including possible loss of principal. Past performance does not guarantee future results. Verify all platforms at sec.gov.ng before investing.