How Childhood Shapes Your Money Beliefs and What to Do About It

Discover how childhood influences money beliefs and learn how to change limiting habits to improve your financial future and build wealth.

Long before you earned your first salary, spent your first naira, or opened your first bank account, your mind was already being programmed with beliefs about money. Understanding where those beliefs came from is the most important financial move you will ever make.

- The Opening Story: Two People, One Income, Two Different Outcomes

- What Are Money Beliefs — and Where Do They Come From?

- How the Brain Builds Money Patterns in Childhood

- The 6 Most Common Childhood Experiences That Shape Adult Money Behaviour

- The 4 Money Scripts — Which One Is Running Your Financial Life?

- The Nigerian Dimension: Money Messages Our Culture Instills in Us

- How to Identify Your Own Money Script

- Rewriting Your Money Story — 7 Practical Steps

- A Reflection Exercise to Start Today

Chidi and Amaka both graduated from the same university, got jobs in the same Lagos firm, and have earned roughly the same salary for the past six years. Today, Amaka owns a flat in Lekki, has ₦3 million in a mutual fund, and is planning to start a business. Chidi cannot explain where his money goes each month. His account is consistently empty three weeks after payday. He feels ashamed to talk about it. He has no savings, no investments, and a growing sense that money is something that happens to other people — not him.

The difference between Chidi and Amaka is not intelligence. It is not discipline in the way most people think. It is something far older, far deeper, and far less visible — the beliefs about money that were installed in each of them before they were ten years old.

1. What Are Money Beliefs and Where Do They Actually Come From?

Every human being walking the earth carries a largely invisible set of beliefs about money. These beliefs govern how you feel when you see your bank balance, whether you feel guilty or proud when you buy something expensive, how you react when someone asks you for your salary, whether you think rich people are admirable or corrupt, and whether you believe, deep down, that wealth is something available to someone like you.

Financial psychologists call these beliefs "money scripts," a term developed by Dr. Brad Klontz and Dr. Ted Klontz in their landmark 2011 study published in the Journal of Financial Therapy. Their research, involving over 400 participants, found that our financial behaviours are far more driven by these unconscious belief patterns than by our knowledge of money, our education, or our income.

The critical insight of this research is where money scripts come from: childhood. These beliefs are typically formed in the earliest years of life, often between ages 3 and 12, and are shaped by what we saw, heard, felt, and experienced around money in our homes, schools, and communities. Most people carry them for their entire adult lives without ever examining them. And they are being passed down generation to generation as automatically and unconsciously as we pass down physical traits.

Research finding: Two people with identical incomes and identical financial literacy can end up in very different financial positions based almost entirely on their emotional relationship with money, not their knowledge of it. Financial education alone is not enough. The psychology must change first.

2. How the Brain Builds Money Patterns in Childhood

To understand why childhood experiences have such a lasting impact on our financial lives, we need to understand a small amount of neuroscience. Children's brains are not miniature adult brains; they are fundamentally different in how they process and store experiences.

The prefrontal cortex, the part of the brain responsible for rational, logical thinking, planning, and impulse control, is not fully developed until a person's mid-twenties. Children experience the world primarily through emotion, sensation, and observation. When a money experience happens in childhood, it is not processed as a logical fact. It is encoded as an emotional memory, often with great intensity.

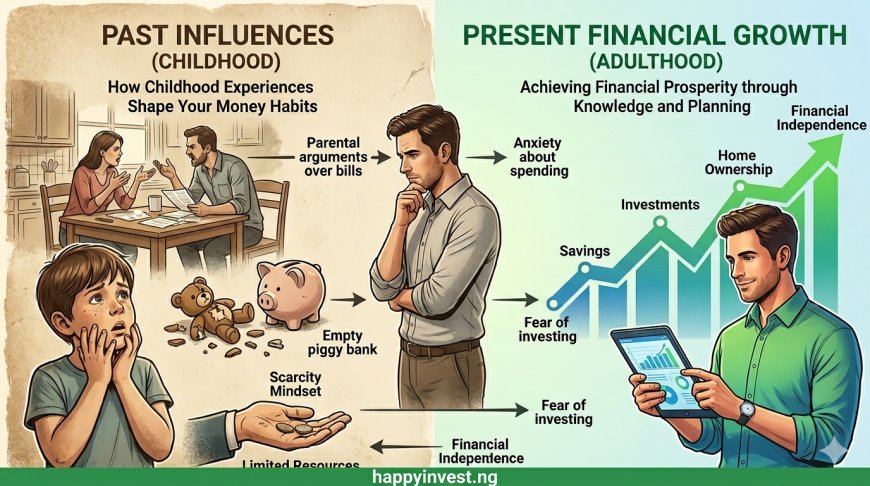

A 6-year-old who watches her parents have a terrifying, screaming argument about unpaid bills does not conclude: "My parents are experiencing temporary cash flow difficulties due to macroeconomic pressures." She concludes, at the level of pure feeling: "Money causes pain. Money destroys love. Money is dangerous." And that conclusion stored in the emotional centres of the developing brain will silently shape every financial decision she makes for the next six decades unless it is consciously examined and rewritten.

Financial psychologist and money coach Mikelann Valterra describes money scripts as things that "run on autopilot in the background," noting that for a money belief to truly stick, there must be a strong emotion associated with it. It is not just watching parents handle money that creates the programming; it is the emotional charge attached to what was witnessed that makes it permanent.

3. The 6 Most Common Childhood Experiences That Shape Adult Money Behaviour

Growing up in financial scarcity or poverty

Children who experience genuine financial hardship, not knowing if there will be food, watching parents stressed about rent, wearing the same worn shoes long after they should have been replaced, often develop what psychologists call a scarcity mindset. As adults, this can manifest as hoarding money fearfully, an inability to invest because "what if I lose it," chronic anxiety about finances even when objectively doing well, or, paradoxically, reckless spending the moment money arrives ("enjoy it before it disappears"). The deep emotional imprint is: there is never enough, and security never lasts.

Witnessing parental conflict about money

Research consistently shows that children who grow up in homes where money is a regular source of conflict and tension between parents often develop money avoidance as adults. They find it difficult to talk about money with partners, avoid opening bills or checking balances, and feel anxious when financial conversations come up. One money coach describes it simply: children who hear their parents fight about money become the adults who, when their partner wants to discuss a budget, "become that 8-year-old again, hearing the arguments, and just want to escape the conversation." This is not weakness; it is a trauma response that was installed decades ago.

Growing up with wealthy parents who never discussed money

A less-discussed dynamic: children who grow up in comfort but where money was never talked about often enter adulthood financially illiterate and emotionally underprepared. Money was simply there; it appeared, it was spent, and nobody explained how it worked or where it came from. These adults frequently struggle with budgeting, have no reference for what things should cost, and may feel vague guilt or unease about their wealth without understanding why. Research confirms that children who had their spending monitored by parents in childhood were significantly more likely to own financial assets and had more positive attitudes toward personal finance as adults. Silence about money is its own form of financial programming.

Being rewarded with money or gifts as a substitute for love or attention

In many Nigerian and African households, particularly those with hard-working parents who are physically present but emotionally absent due to long working hours, children learn to associate money and material gifts with love. When a parent is too busy to attend your school play but brings you a new toy instead, the developing brain writes a script: money = love, purchases = comfort, shopping = emotional regulation. As adults, these individuals often become compulsive spenders, reaching for purchases not because they want the item, but because buying something temporarily fills an emotional void. This is one of the most common and least understood patterns behind adult financial self-sabotage.

Being explicitly taught that money is evil, shameful, or dangerous

Religious and cultural teachings that frame wealth as morally suspect, such as "money is the root of all evil," "rich people are corrupt," and "being poor is humble and virtuous," plant deep money avoidance scripts that can cripple financial ambition for life. The person who grows up hearing these messages and then earns a good salary faces an internal psychological conflict: to accumulate wealth is to become the kind of person they were taught to distrust. This inner conflict often results in unconscious self-sabotage, overspending, over-giving, undercharging for services, or avoiding investments, all in service of a childhood belief that money itself is something to be kept at a distance.

Being raised in a household where social status was tied to money and appearances

Families where money was used to signal status, where what the neighbours thought mattered intensely, where the car, the clothing brand, the neighbourhood all communicated social standing, produce adults who struggle to distinguish between spending for genuine value and spending for appearances. These individuals often buy things they cannot afford to impress people they may not even like, carry credit card debt to maintain a lifestyle image, and feel secretly inadequate regardless of how much they earn. The childhood script installed: your worth as a person is measured by what you visibly possess.

4. The 4 Money Scripts: Which One Is Running Your Financial Life?

Based on their research with over 400 people, financial psychologists Klontz and Klontz identified four distinct money belief patterns that the vast majority of people fall into. These are not personality types — they are learned patterns, formed in childhood, that can be unlearned. Research found that three of the four scripts are directly associated with poorer financial health, including lower net worth and lower income.

"Money is bad. Rich people are greedy. I don't deserve wealth."

Money avoiders believe wealth is morally corrupting and that good, virtuous people should not desire or accumulate it. They often give money away before they can save it, avoid looking at their accounts, undercharge for their work, self-sabotage financial progress, and feel intense guilt around prosperity. This script frequently develops in homes where money was portrayed as dangerous or shameful, or where religious teachings equated poverty with virtue.

In Nigeria, this sounds like: "I don't want to become like those people." / "God will provide, I shouldn't chase money." / "I feel guilty charging my friends." / "The more I earn, the more problems I have."

"More money will solve all my problems. I will finally be happy when I have enough."

Money worshippers believe that wealth is the solution to all life's difficulties, emotional, relational, and existential. The tragic irony is that people with this script never have "enough." They pursue money compulsively, often prioritize work over relationships, may gamble or make high-risk financial decisions chasing a windfall, and spend impulsively trying to fill an emotional hole with purchases. This script often develops when a family experiences genuine hardship, creating an overvaluation of wealth as the answer to all suffering.

In Nigeria, this sounds like: "Once I make it big, all my problems go away." / "I just need one big deal and life changes." / Monthly salary spent in 2 weeks on lifestyle items with nothing saved.

"My net worth is my self-worth. What I own tells people who I am."

People with the money status script have deeply fused their identity and social value with their visible wealth. They buy not for joy but for signalling. They overspend on cars, clothing, and gadgets to project an image of success. They may carry significant debt while maintaining the appearance of prosperity. Research found that people with this script tend to have lower levels of education, income, and net worth — yet spend beyond their means to appear otherwise. They often keep their actual finances secret, even from spouses.

In Nigeria, this sounds like: "I must wear the right brands." / "People respect me because of my car." / Spending a month's salary on a party to maintain an image. / Deep discomfort with people knowing the truth of your finances.

"Save everything. Never waste. Be careful — security can disappear at any moment."

This is the only script associated with better financial health outcomes. The money vigilant prioritize saving, live within their means, and are cautious with debt. However, taken to an extreme, this script creates its own problems: excessive anxiety about money, even when objectively secure, inability to enjoy spending, hoarding, and difficulty giving generously or investing because of fear of loss. The healthy version of this script is the foundation of wealth-building; the unhealthy version is a prison of chronic financial anxiety.

In Nigeria, this sounds like: "Don't tell anyone how much you earn." / "Save before you spend anything." / Refusing to enjoy the rewards of hard work out of fear. / Extreme discomfort with any financial risk, even low-risk investments.

Important: Most people carry a mix of scripts, not a pure version of one. You may be primarily money vigilant with strong money status elements, or money avoidant with money worship tendencies. The goal is not to label yourself but to begin seeing your patterns clearly.

5. The Nigerian Dimension: Money Messages Our Culture Instills in Us

Beyond the universal psychological dynamics, Nigerians and West Africans grow up with a specific set of cultural money messages that deserve direct examination because they are so deeply embedded in our daily life that we rarely recognize them as beliefs at all. We simply think of them as "how things are."

Money Scripts Unique to the Nigerian Experience

"You must take care of everyone." The Family Obligation Script

Many Nigerians grow up in extended family systems where financial success is immediately and automatically shared with parents, siblings, aunts, uncles, and cousins. The message instilled is: your money is the family's money. While this reflects genuine communal values, it also creates a devastating financial pattern for the individual — the inability to save or invest because every surplus is immediately redistributed. Adults carrying this script often earn well but accumulate nothing, because the social pressure to give is experienced as an identity-level obligation, not a choice. They cannot distinguish between healthy generosity and self-destructive over-giving.

"Show people you have arrived." The Aso-Ebi and Owambe Economy

Nigerian social culture places extraordinary pressure on conspicuous spending as proof of success and belonging. Owambe parties, matching fabric purchases, naming ceremonies, and lavish celebrations create a social expectation that money, when present, must be seen to be present. Children growing up in this environment learn that spending publicly is how you maintain respect and social standing, while saving quietly is invisible and therefore unrewarded socially. This installs the money status script powerfully and early, making it exceptionally difficult for young Nigerian adults to prioritize wealth-building over wealth-displaying.

"Money talk is rude": The Financial Secrecy Script

In many Nigerian households, discussing money openly — asking what someone earns, talking about debts, admitting financial difficulty- is considered deeply inappropriate. Children learn that money is a private matter, almost a shameful one. As adults, this creates an inability to have honest financial conversations with partners, families, or advisors; a reluctance to seek help when in financial difficulty; and a pattern of financial secrecy that prevents accountability and growth. Many Nigerians carry significant financial stress entirely alone because they were taught that admitting financial struggle is a form of social failure.

"Work hard, and God will bless you" — The Passive Abundance Script

Faith is central to Nigerian life, and the belief that financial prosperity is God's blessing in response to spiritual faithfulness is widespread and genuine. The problematic version of this belief, however, passively waits for divine intervention while avoiding the active, strategic financial planning that actually builds wealth. Children raised in households where financial success was attributed entirely to prayer and divine favour — with little discussion of budgeting, investing, or building skills — may grow up believing that planning their finances is somehow a lack of faith, rather than the responsible stewardship of the resources they have been given.

"The rich got there by stealing" — The Corruption Script

In a country with visible and painful wealth inequality and a long history of leadership corruption, many Nigerians grow up with the deeply held belief that great wealth and moral integrity cannot coexist, that any significantly wealthy person must have gotten there through dishonesty. While this reflects real and legitimate frustrations with systemic inequality, it also installs a money avoidance script that makes genuine wealth-building feel like a moral compromise. Young Nigerians carrying this belief unconsciously self-limit their financial ambitions to stay "one of the good people."

6. How to Identify Your Own Money Script

Recognition is the beginning of everything. Before you can rewrite a pattern, you must first be able to see it clearly. Here is how to begin that process honestly:

Look at your financial behaviour, not your intentions

Your money script reveals itself not in what you plan to do but in what you actually do consistently, repeatedly, over the years. Do you earn well but consistently have nothing saved? Do you feel physical anxiety when you check your bank balance? Do you spend significantly on things that matter to other people's perception of you, while cutting corners on things that would genuinely improve your life? Do you lend money you cannot afford to lend? Do you feel guilty charging appropriately for your work? These are not character flaws. They are the footprints of a childhood belief system that is still running.

Trace your earliest money memories

Sit quietly and ask yourself: What is my earliest memory involving money? What feelings does it carry? What was the emotional atmosphere of money in your home growing up? Was it discussed openly or treated as taboo? Was it a source of tension or pride? What did your parents say about wealthy people? What did they say about poor people? What were the unspoken rules about how money should be earned, spent, saved, and discussed in your family? The answers to these questions are a map of your current financial behaviour.

Notice your emotional reactions around money

The most revealing test is simply paying attention to how money makes you feel, not what you think about it intellectually, but how your body responds. Anxiety when your account is full? Money avoidance. A compulsive urge to spend immediately after receiving money? Likely a scarcity script or money worship. Intense discomfort when someone asks what you earn. Money status or financial secrecy script. Physical tension when anyone asks you to discuss budgets? Childhood conflict association. Emotions are the language of money scripts; they are where the childhood programming most clearly speaks.

7. Rewriting Your Money Story — 7 Practical Steps

Identifying your money script is profound, but it is only the beginning. The real work is in the deliberate, consistent process of creating new associations, new beliefs, and new behaviours. Here is a practical framework for doing so:

1. Name the script explicitly, write it down

The most powerful first step is to take your unconscious belief and make it fully conscious by writing it down as a statement. "I believe money is dangerous and people who want a lot of it are greedy." Seeing the belief written down in plain language immediately begins to loosen its hold, because our rational minds can then engage with it as a belief, something that was learned, rather than as an obvious fact about reality. Write the belief. Then write where it came from: which parent said it, what specific event encoded it, and which experience first made you feel this way about money.

2. Challenge the belief with evidence

Using cognitive restructuring, a technique from cognitive behavioural therapy, ask yourself: what is the actual evidence for and against this belief? If your belief is "rich people are greedy and corrupt," can you think of wealthy people you personally know or know of who are generous, ethical, and admirable? The goal is not to replace one extreme belief with another, but to introduce nuance and complexity where your childhood installed a simplistic rule. Most childhood money beliefs are, as researchers describe them, "partial truths." They contain a seed of real experience, but were overgeneralized by a young mind trying to make sense of the world.

3. Separate your parents' story from your story

The beliefs you absorbed in childhood were not necessarily wrong for your parents, given their circumstances, experiences, and the era they lived in. A parent who survived extreme poverty may have developed extreme frugality as a genuinely adaptive survival response. A parent who grew up with nothing and witnessed corruption may have a legitimate reason for distrusting wealth. Your task is not to judge their script but to consciously decide whether it serves your life and your goals. You inherited their programming; you were never asked if you wanted it. Now, as an adult, you can choose to keep what serves you and deliberately release what does not.

4. Create new, deliberate financial experiences

Beliefs change through experience more reliably than through intellectual argument alone. If you carry financial anxiety, deliberately practise small acts of financial confidence, opening your investment app and not closing it immediately, setting a savings goal and hitting it, making one investment, no matter how small. Each positive experience creates a new data point that challenges the old belief. Children who owned savings accounts in childhood were significantly more likely to own financial assets as adults, not because of the money in the account, but because of the experience of managing money successfully, which created a new belief: I am someone who can do this.

5. Set clear, personal boundaries around the family obligation script

For Nigerians specifically, this is often the single most financially consequential step. This does not mean abandoning your family or refusing to help people you love. It means distinguishing between help you genuinely choose to give from a place of abundance and help you feel coerced into giving out of guilt or fear of social judgment. You cannot build wealth while handing away every surplus the moment it appears. Decide deliberately what proportion of your income you will give, then protect the rest with the same intentionality you would protect your health or your most important relationships. Generosity chosen freely is a value. Generosity extracted under social pressure is a financial drain, regardless of how it is dressed up culturally.

6. Talk about money openly, break the silence script

In a culture where money talk is taboo, deliberately choosing to have honest financial conversations is a radical and powerful act of reprogramming. Talk to your partner about money, not just logistics, but feelings, fears, and goals. Find one friend you trust enough to be honest with about your financial situation. Consider joining or creating a small investment group where finances are discussed openly and without shame. The simple act of speaking about money without fear or shame begins to dissolve the childhood association between financial honesty and social danger.

7. Consider working with a financial therapist or counsellor

Financial therapy is a growing field that specifically addresses the psychological roots of money behaviour, combining the tools of traditional therapy with financial planning expertise. If your money patterns have caused significant harm in your life, destroyed relationships, prevented wealth-building despite good income, created chronic anxiety or shame, a financial therapist can help you trace these patterns to their roots and create genuinely new responses. This is not a luxury for the privileged. It is, for many people, the most practical financial investment they can make.

8. A Reflection Exercise to Start Today

You do not need a therapist to begin this process. The following questions, taken seriously and answered honestly in writing, not just in your head, can begin to reveal the money scripts that have been operating silently in your financial life for years.

Your Money Story Reflection

What is your earliest memory that involves money? What feelings does that memory carry?

When you were growing up, was money discussed openly at home, or was it treated as a sensitive, shameful, or forbidden topic?

What did your parents through their actions, not just their words teach you about wealth? About poor people? About rich people?

Did you ever experience genuine financial scarcity as a child? If so, how do you think that experience still lives in your body today when you feel financially uncertain?

How does money make you feel today when you have it, when you don't, when you spend it, when you save it? Be specific about the feelings, not the thoughts.

Do you know of any family beliefs about money that were passed down from your grandparents' generation? How might those beliefs live in you today?

What would your financial life look like right now if you truly believed at the deepest level that you deserved financial abundance and were capable of creating it?

What is one money belief you are ready to consciously release, and what new belief would you choose to replace it with?

The Most Important Financial Education Begins With You

Every financial book, every investment app, every savings tip and stock market strategy in the world will struggle to deliver its full value if the psychological programming underneath it is working against you. You can know exactly how compound interest works and still spend every naira the moment it arrives because a part of you learned in childhood that money is dangerous and should be dispersed before it causes trouble.

The good news, backed by decades of research in financial therapy and psychology, is that money scripts formed in childhood can be identified, challenged, and, over time, genuinely rewritten. Not perfectly. Not overnight. But with patient, honest, deliberate attention to the beliefs running silently in the background of every financial decision you make.

Chidi and Amaka, from the story at the beginning of this article, were not fated to their different outcomes by talent or luck. They were shaped by invisible scripts installed before they were old enough to choose. But here is what psychology also tells us: awareness is the beginning of freedom. The script is not destiny. It is the starting point of a different story, one you now have the power to consciously write.

Your action step today: Take 20 minutes with the reflection questions above. Write your answers in a notebook, not on your phone. Be brutally honest. Identify which of the four money scripts feels most familiar. Write down one belief about money you inherited from your childhood that you are choosing, today, to consciously examine. That single act of awareness is the beginning of your real financial education.

This article draws on research from the Journal of Financial Therapy, behavioural finance literature, and financial psychology. It is for educational and self-reflection purposes only. For significant financial or psychological distress, please consult a licensed financial therapist or mental health professional.