Rebalancing Your Portfolio: When to Sell and When to Buy More

Understand portfolio rebalancing, when to sell, and when to buy more investments. Learn how to manage risk and improve returns with a disciplined strategy. Learn what portfolio rebalancing is, why it matters, and when to sell or buy more investments to maintain a balanced and profitable portfolio.

Many people focus on what to invest in, but very few understand something equally important:

How to manage your investments after you’ve started.

Markets move. Prices change. Some investments grow faster than others. Over time, your portfolio can drift away from your original plan.

This is where portfolio rebalancing becomes essential.

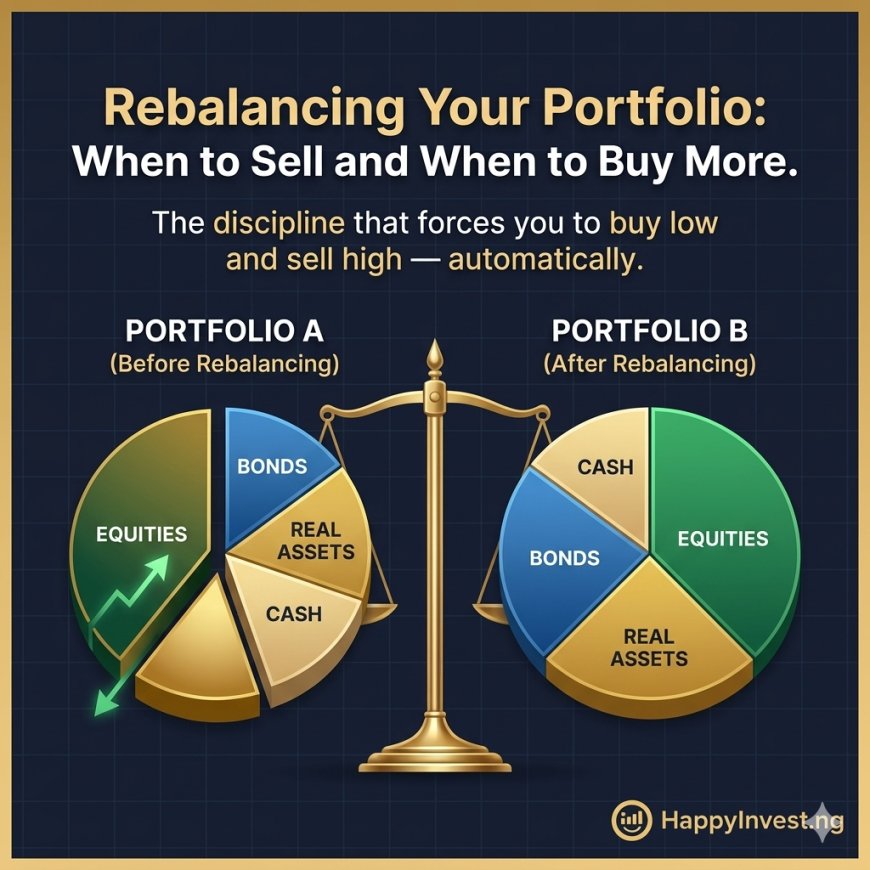

What Is Portfolio Rebalancing? (Simple Definition)

Portfolio rebalancing is the process of adjusting your investments to maintain your desired asset allocation.

In simple terms:

You periodically sell some investments and buy others to keep your portfolio balanced according to your plan.

Why Rebalancing Matters

Without rebalancing, your portfolio can become:

-

Too risky

-

Too concentrated in one asset

-

Misaligned with your goals

Example

You start with:

-

50% stocks

-

30% fixed income

-

20% crypto

After one year:

-

Stocks perform well → now 70%

-

Crypto drops → now 10%

Your portfolio is now riskier than you planned.

Rebalancing helps you bring it back to your original structure.

When Should You Rebalance Your Portfolio?

There is no one-size-fits-all answer, but here are the most effective approaches:

1. Time-Based Rebalancing

You rebalance at regular intervals:

-

Every 3 months

-

Every 6 months

-

Once a year

This method is simple and works well for beginners.

2. Threshold-Based Rebalancing

You rebalance when your allocation changes beyond a certain level.

Example:

-

If any asset moves more than 5–10% from your target

This method is more precise and keeps your risk under control.

3. Life Event Rebalancing

You rebalance when your situation changes:

-

New job or income

-

Marriage or family responsibilities

-

Financial goals change

When to Sell and When to Buy More

This is where many investors struggle emotionally.

When to Sell

You should consider selling when:

1. An Asset Has Grown Too Much

If one investment becomes too large in your portfolio:

-

It increases risk

-

You may be overexposed

Rebalancing means:

Sell part of it and redistribute.

2. Your Investment Thesis Has Changed

If the reason you invested is no longer valid:

-

Poor company performance

-

Industry decline

-

Economic changes

Then selling is justified.

3. You Need to Reduce Risk

As you approach financial goals:

-

Reduce exposure to volatile assets

-

Increase safer investments

When to Buy More

You should consider buying more when:

1. An Asset Has Dropped but Still Has Value

Market declines can create opportunities.

If fundamentals remain strong:

-

Prices are lower

-

Future growth potential remains

This is where disciplined investors take advantage.

2. Your Allocation Is Too Low

If an asset falls below your target percentage:

-

Rebalancing requires buying more

3. Long-Term Strategy Remains Intact

If nothing has changed fundamentally:

-

Market drops should not scare you

-

They can be opportunities

The Psychology of Rebalancing

Rebalancing often feels uncomfortable because it requires you to:

-

Sell what is performing well

-

Buy what is underperforming

This goes against human instincts.

Most people:

-

Chase winners

-

Avoid losers

But disciplined investors:

-

Lock in gains

-

Buy undervalued assets

Real-Life Example (Nigeria Context)

Imagine two investors:

Investor A (No Rebalancing)

-

Invests in stocks, crypto, and fixed income

-

Ignores portfolio changes

-

Ends up heavily exposed to one asset

Result:

-

High risk

-

Unstable performance

Investor B (Rebalances Regularly)

-

Reviews portfolio every 6 months

-

Adjusts allocations

-

Maintains balance

Result:

-

Controlled risk

-

More stable growth

Simple Rebalancing Strategy for Beginners

If you are just starting, use this:

-

Set your target allocation

-

Example:

-

50% stocks

-

30% fixed income

-

20% crypto

-

-

-

Review every 6 months

-

Rebalance if any asset deviates by more than 5–10%

-

Sell high-performing assets slightly

-

Buy underperforming assets carefully

Common Mistakes to Avoid

-

Rebalancing too frequently

-

Ignoring transaction costs

-

Letting emotions guide decisions

-

Holding losing investments without reason

-

Selling strong investments too early

How Rebalancing Protects Your Wealth

Rebalancing helps you:

-

Control risk

-

Avoid overexposure

-

Maintain discipline

-

Improve long-term returns

It ensures your portfolio stays aligned with your goals.

Discipline Beats Emotion

Successful investing is not just about:

-

Picking the right assets

It is about:

-

Managing them properly over time

Rebalancing teaches one powerful principle:

Buy low, sell high, but in a structured and disciplined way.

If you apply this consistently, you:

-

Reduce risk

-

Stay in control

-

Build wealth more sustainably