How to Design Your Personal Money System

Learn how to design a personal money system that helps you manage income, control spending, save consistently, and build long-term wealth. Create a powerful personal money system to manage your finances, save consistently, and build wealth. A simple guide for financial success.

Most people don’t have a money problem.

They have a money system problem.

They earn income…

They spend…

They try to save what’s left…

And at the end of the month, nothing remains.

If you want to build real wealth, you need more than motivation.

You need a system that manages your money automatically and consistently.

What Is a Personal Money System? (Simple Definition)

A personal money system is a structured way of managing your income, expenses, savings, and investments.

In simple terms:

It is how your money flows from when it enters your account to how it is used.

Why You Need a Money System

Without a system:

-

You rely on discipline alone

-

You make emotional decisions

-

Your money disappears without direction

With a system:

-

Your money has a plan

-

Your priorities are clear

-

Wealth-building becomes consistent

Step 1: Know Your Financial Numbers

You cannot build a system without clarity.

Start by identifying:

-

Monthly income

-

Fixed expenses (rent, food, transport)

-

Variable expenses (entertainment, shopping)

-

Current savings

Why This Matters

You need to know:

What is coming in and what is going out

Step 2: Define Your Financial Goals

Your system must be built around your goals.

Examples:

-

Emergency fund (3–6 months of expenses)

-

Buying a house

-

Investing for long-term wealth

-

Starting a business

Key Principle

Your goals determine how your money should be allocated.

Step 3: Create a Simple Allocation Structure

This is the foundation of your system.

A simple structure could be:

-

50% → Living expenses

-

20% → Savings

-

20% → Investments

-

10% → Personal spending

Adjust Based on Your Reality

Your percentages may differ, but the key is:

Every naira must have a purpose.

Step 4: Pay Yourself First

Do not save what is left after spending.

Instead:

-

Save immediately after receiving income

This ensures:

-

Your financial goals are prioritized

-

You build consistency

Step 5: Automate Your Money Flow

Automation reduces the need for discipline.

Set up:

-

Automatic transfers to savings

-

Scheduled investment contributions

Why It Works

-

Removes temptation

-

Builds consistency without effort

Step 6: Separate Your Accounts

One of the most effective strategies is account separation.

Use different accounts for:

-

Spending

-

Savings

-

Investments

Benefit

You avoid mixing money and overspending.

Step 7: Build an Emergency Fund

Before aggressive investing, build a safety net.

Target:

-

3–6 months of expenses

This protects you from:

-

Unexpected expenses

-

Selling investments at the wrong time

Step 8: Create a Simple Investment Plan

Your system should include investing.

Decide:

-

What to invest in (stocks, fixed income, etc.)

-

How often to invest

-

How much to invest

Key Rule

Consistency matters more than timing.

Step 9: Review and Adjust Regularly

Your system is not static.

Review:

-

Monthly spending

-

Savings progress

-

Investment performance

Adjust when necessary:

-

Income changes

-

Goals change

-

Life circumstances change

Step 10: Keep It Simple

A complex system is hard to maintain.

The best money system is:

-

Simple

-

Clear

-

Easy to follow

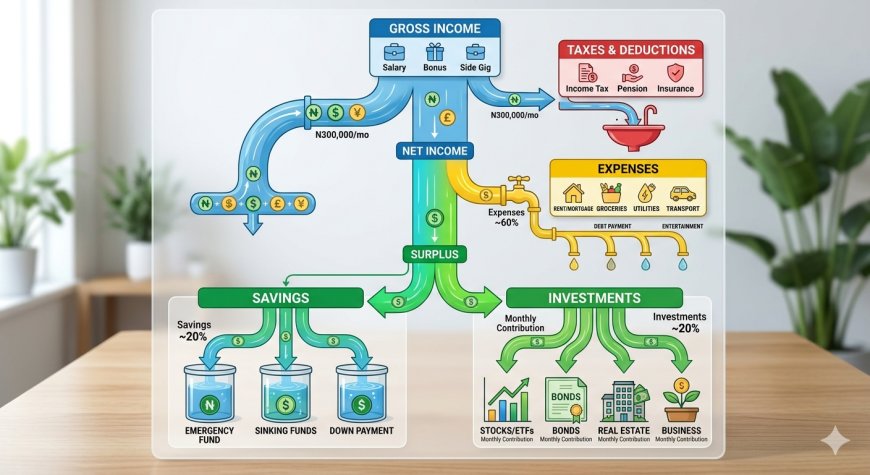

Example of a Simple Personal Money System

Income: ₦300,000/month

-

₦150,000 → Expenses

-

₦60,000 → Savings

-

₦60,000 → Investments

-

₦30,000 → Personal use

This system:

-

Creates balance

-

Ensures consistency

-

Supports long-term growth

Common Mistakes to Avoid

-

Not tracking income and expenses

-

Saving inconsistently

-

Mixing all the money in one account

-

Overcomplicating the system

-

Ignoring long-term goals

Real-Life Comparison

Person A (No System)

-

Spends first

-

Saves randomly

-

No investment structure

Person B (With System)

-

Follows a structured plan

-

Saves and invests consistently

-

Tracks financial progress

After a few years:

-

Person A struggles financially

-

Person B builds stability and wealth

Benefits of a Personal Money System

-

Financial clarity

-

Better decision-making

-

Reduced stress

-

Consistent wealth building

-

Control over your finances

Systems Create Results

Motivation comes and goes.

But a system:

-

Works every month

-

Builds discipline automatically

-

Creates long-term results

If you want to change your financial life:

Do not rely on willpower.

Build a system that works for you.