What Is Asset Allocation and Why It Matters for Your Portfolio

What is asset allocation, and why does it matter more than picking the right stocks? Happyinvest breaks down asset allocation for Nigerian investors with three model portfolios, real naira examples, how to rebalance, and a step-by-step guide to building your first intentional investment portfolio in Nigeria. A must-read for intermediate investors.

Making Money Simple. Building Wealth Daily.

Let me ask you something real.

You've been investing for a while now, or at least thinking about it seriously. You have some money in a money market fund. Maybe you've bought a few stocks. Perhaps you opened a Bamboo account and bought a little S&P 500. You're doing something. And that's genuinely good.

But here's the question I want you to sit with for a moment:

Do you have a plan for how you divide your money, or are you just putting it wherever it feels right at the time?

If you're honest and the answer is "wherever feels right," you're not alone. Most Nigerian investors at the beginning to intermediate stage are investing by feel. A little here. A little there. Follow what someone on Twitter recommended. Put more in when the market is doing well. Freeze when things go south.

That's not a strategy. That's financial instinct, and financial instinct without a framework will cost you money over time.

What you're missing is something called asset allocation. And I want to tell you today, clearly, practically, without any jargon, exactly what it is, why it might be the most important investment concept you'll ever learn, and how to build it correctly for your own life.

This is the article that will help your investing graduate from "I'm doing something" to "I have a real, intentional portfolio." Let's get into it.

What Is Asset Allocation?

Asset allocation simply means: how you divide your investment money across different types of assets.

That's it. That's the whole concept at its core.

Instead of putting all your money in one place, all in stocks, or all in treasury bills, or all in a money market fund, you deliberately spread it across several different asset types in specific proportions. Each type of asset plays a different role in your portfolio. Together, they balance each other out.

Let me use a food analogy because this is Nigeria, and we understand food deeply.

Think of your investment portfolio like a balanced plate of food. You need carbohydrates for energy, that's your growth assets, like stocks. You need protein for strength, that's your fixed income, like bonds and Tbills. You need vegetables for stability and health, that's your cash and money market funds. And you need fat for long-term fuel, that's your real estate and alternative assets.

If you eat only carbs, you'll get a sugar spike and crash. If you eat only vegetables, you'll be stable but not strong enough. A balanced plate gives you everything your body needs to function well over the long run.

Your investment portfolio works exactly the same way. Asset allocation is how you build a balanced portfolio for your money.

The Asset Classes: Understanding Your Ingredients

Before you can allocate properly, you need to understand what the different asset classes actually are and what role each plays. For a Nigerian investor in 2026, here are the main ones.

Cash and Money Market Funds

This is the safest layer of your portfolio. Money market funds, savings accounts, and similar instruments preserve your capital while earning modest but reliable returns. In Nigeria right now, top money market funds yield 18–22% per annum, which is genuinely impressive for a "safe" category. These are your most liquid assets you can access them within 24–72 hours.

Their role in your portfolio: stability, liquidity, and emergency access. They're not where you build dramatic wealth; they're where you park money that needs to be safe and accessible.

Fixed Income Treasury Bills and Bonds

These are government or corporate debt instruments. When you buy a treasury bill or an FGN bond, you're essentially lending money to the Nigerian government for a fixed period and collecting interest. Currently, Nigerian Tbills yield around 20–22% per annum. FGN bonds offer similar or slightly different rates depending on the tenor.

Their role in your portfolio: predictable, stable returns that are slightly better than money market funds, with a fixed timeline. They add structure to your portfolio and reduce overall volatility.

Nigerian Stocks (Equities)

When you buy shares of companies listed on the Nigerian Exchange Group (NGX), you're owning a piece of those businesses. Quality Nigerian stocks GTCO, Zenith Bank, MTN Nigeria, BUA Foods, Dangote Cement have historically delivered strong longterm returns through price appreciation and dividends.

Their role in your portfolio: growth. Stocks are the primary engine for building real wealth over time. They're more volatile than fixed income; they go up and down with market conditions, but over 5–10 year horizons, quality stocks typically outperform every other naira asset class.

Dollar Assets US Stocks and ETFs

Accessed through platforms like Bamboo, Chaka, Trove, and Risevest, dollar investments give you exposure to the US stock market. The S&P 500, which tracks America's 500 largest companies, has averaged roughly 10–12% returns annually in USD terms over decades. On top of that return, you benefit from any naira depreciation against the dollar, a very real and recurring feature of the Nigerian economic environment.

Their role in your portfolio: growth plus currency protection. Dollar assets are one of the most powerful tools an educated Nigerian investor has for preserving and growing wealth against naira devaluation.

Real Estate and REITs

Physical property, land, residential buildings, and commercial property are a major wealth class in Nigeria. But direct real estate requires significant capital and is illiquid. Real Estate Investment Trusts (REITs) listed on the NGX, like UPDC REIT, solve both problems; they give you exposure to real estate returns with much lower capital requirements and full liquidity.

Their role in your portfolio: tangible asset exposure, rental income distribution, and inflation protection. Real estate tends to appreciate over time and often moves independently of the stock market, which is exactly what you want for diversification.

Alternative Assets

This category includes things like commodities (gold, oil), private equity, and, for those who understand the risks, certain crypto assets. These are generally not starter positions for most Nigerian investors. They're supplementary assets added to a mature portfolio to enhance diversification further.

Their role in your portfolio: additional diversification and inflation hedging. Best added after the core portfolio is well-established.

Why Asset Allocation Matters More Than Which Stocks You Pick

Here's a fact that surprises most people when they first hear it.

Research in global financial markets consistently shows that over 90% of a portfolio's longterm performance is determined by asset allocation, not by which specific stocks you pick or when you buy and sell.

Let me say that again because it's that important.

Picking Apple over Microsoft, or Zenith over GTCO, matters far less than the question of how much of your total portfolio is in stocks versus bonds versus cash versus dollar assets.

Most beginner investors spend the majority of their energy asking "which stock should I buy?" when the more important question is "how should I divide my money across different asset types?"

This is why two people can both "invest in stocks" and get completely different results. Person A puts 90% of their portfolio in Nigerian stocks with no diversification. When the NGX has a bad year, its entire portfolio suffers. Person B has 35% in Nigerian stocks, 25% in US dollar assets, 20% in fixed income, and 20% in money market funds. When the NGX dips, their fixed income and dollar holdings cushion the blow. Person B sleeps better. Person B's portfolio is more resilient. And over time, Person B's risk-adjusted returns tend to be better.

Asset allocation is the architecture of your portfolio. You can put great furniture in a badly designed building, and it still won't work properly. But get the architecture right and even modest furnishings produce a comfortable, functional space.

The Three Forces That Should Drive Your Allocation Decision

Here's the practical question: how do you know what allocation is right for YOU?

There are three main factors that determine the right asset allocation for any individual investor. Get honest with yourself about each one.

Force 1: Your Time Horizon

How long can you leave your money invested without needing to touch it?

This is the single most important factor. Here's why: the longer your time horizon, the more risk you can afford to take because time smooths out volatility.

A 25yearold investing for retirement 35 years away can afford to have 70% of their portfolio in growth assets like stocks. If the market drops 30% next year, they have 34 more years for it to recover and continue compounding. They have time on their side.

A 45yearold saving for their child's university fees that start in 3 years cannot put that money in volatile stocks. If the market drops 30% next year, they need that money in 2 years. They cannot afford to wait for recovery. Their time horizon is short, so they need a more conservative allocation.

The rule of thumb: shorter timeline = more conservative allocation (more cash and bonds, fewer stocks). Longer timeline = more aggressive allocation (more stocks and growth assets, less cash and bonds).

Force 2: Your Risk Tolerance

Risk tolerance is your emotional and financial ability to handle your portfolio losing value temporarily without doing something irrational like panicking and selling.

Two people can have identical time horizons and still need different allocations based on risk tolerance.

Some people can watch their portfolio drop 30% and stay completely calm. They understand it's temporary, they keep contributing, and they don't sell. These people have high risk tolerance and can handle aggressive allocations with lots of stock exposure.

Other people watch their portfolio drop 15% and feel physically sick. They can't sleep. They want to sell everything. These people have low risk tolerance, and no matter how long their time horizon is, an aggressive allocation will cause them to make emotional decisions that destroy their returns. They need a more conservative allocation that they can actually stick to.

Be honest about which type you are. There's no shame in low risk tolerance; in fact, knowing it and building your portfolio around it is a sign of wisdom, not weakness. An investment plan you can actually follow beats a theoretically perfect plan you'll abandon the moment markets get choppy.

Force 3: Your Financial Goals

Different goals require different allocations.

Building retirement wealth over 25 years? Heavy growth allocation lots of stocks, lots of dollar assets, minimal cash drag.

Saving for your child's university fees starting in 5 years? Moderate allocation of some growth assets for the first 3 years, shifting toward conservative as the goal approaches.

Building your emergency fund? Conservative allocation only to money market funds and Tbills. Zero stock exposure for this specific money.

Saving for a land purchase in 18 months? Ultraconservative Tbills and money market funds. This is not money that should be in stocks.

The key insight here is that you might have multiple goals running simultaneously, and each goal should have its own allocation, not one portfolio trying to serve all purposes at once.

The Three Model Portfolios Find Your Starting Point

Based on the three forces above, here are three model portfolio allocations for Nigerian investors. These are starting frameworks, not rigid rules. Your personal situation will require adjustments.

Model 1: The Conservative Portfolio

Best for: Short timelines (1–3 years), low risk tolerance, specific near-term goals

40% in money market funds, your liquid, safe foundation 40% in treasury bills and FGN bonds, stable, government-backed returns 10% in Nigerian quality stocks, just enough equity exposure for some growth 10% in dollar assets via a managed plan like Risevest, basic currency protection

This portfolio will not make you rich quickly. But it will preserve your capital, beat inflation comfortably at current Nigerian rates, and let you sleep at night. Perfect for someone building an emergency fund, saving for a specific goal, or who is genuinely uncomfortable with volatility.

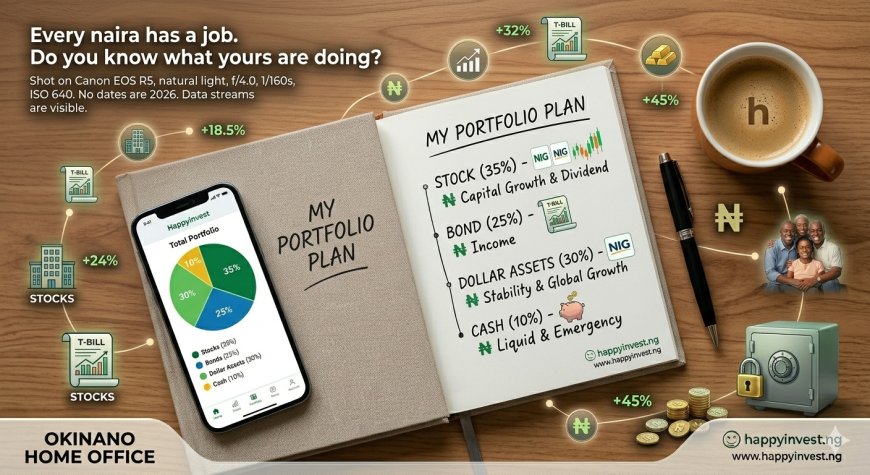

Model 2: The Balanced Portfolio

Best for: Medium timelines (3–7 years), moderate risk tolerance, wealth building with some near-term needs

20% in money market funds, your liquid cushion, 25% in fixed income (T-bills and bonds), stability anchor, 25% in Nigerian stocks (quality blue chips and equity mutual funds), naira growth engine, 20% in US stocks and ETFs via Bamboo or Trove dollar growth, and naira hedge, 10% in REITs, real estate exposure without the capital burden

This is the most versatile portfolio model for the average Nigerian intermediate investor. It has real growth potential through stocks and dollar assets, meaningful stability through fixed income, and genuine liquidity from the money market layer. This is where most working Nigerians between 25 and 40 with stable income should be building.

Model 3: The Aggressive Portfolio

Best for: Long timelines (7+ years), high risk tolerance, serious long-term wealth building

10% in money market funds, emergency access only 10% in fixed income, minimum stability layer 35% in Nigerian stocks and equity mutual funds, primary naira growth engine 30% in US stocks and ETFs, primary dollar wealth builder 15% in REITs and real estate tangible asset diversification

This portfolio is for the investor who has time on their side, understands that short-term volatility is the price of long-term returns, and is committed to not touching this money for at least 7 years. Over a 15–20 year period, this aggressive allocation, properly managed and consistently contributed to, has the potential to produce life-changing wealth.

The Concept That Holds It All Together: Diversification

You've probably heard "don't put all your eggs in one basket" a hundred times. That's diversification in a sentence. But let me explain why it actually works mathematically, because understanding the why will make you take it far more seriously.

Different asset classes have something called low correlation with each other. This means they don't move in exactly the same direction at the same time.

When Nigerian stocks are having a bad year because of local economic pressure, US stocks might be doing well different economy, with different drivers. When interest rates rise and bond prices fall, your money market fund returns might actually improve. When the naira weakens, your dollar assets in naira terms actually gain value.

By holding assets that respond differently to economic conditions, you ensure that something in your portfolio is always performing reasonably well, even when something else is struggling. Your overall portfolio volatility drops dramatically. Your returns become smoother and more consistent.

This is not just theory. This is the mathematical foundation of modern portfolio management. It's why institutional investors, pension funds, sovereign wealth funds, and endowments all allocate across multiple asset classes rather than concentrating in one.

You don't need to be a pension fund manager to apply this principle. You just need to intentionally spread your money across the asset classes available to you in Nigeria, which we've now clearly laid out.

Rebalancing The Discipline That Keeps Your Portfolio Honest

Here's something most beginner investors don't know about: rebalancing.

Over time, your portfolio will drift from its original allocation. This happens naturally because different assets grow at different rates.

Let's say you start with a balanced portfolio: 25% Nigerian stocks, 25% fixed income, 20% dollar assets, 20% money market, 10% REITs.

After two years of strong performance, your Nigerian stocks have grown dramatically and now represent 40% of your portfolio. Your fixed income, which grew more slowly, is now only 15%. Your dollar assets are 30%. Your portfolio has drifted significantly from where you intended it to be.

This matters for two reasons. First, you're now taking on more risk than you planned. Your portfolio is now stock-heavy in a way that wasn't intentional. Second, you've lost the diversification balance that protects you.

Rebalancing means periodically, typically every 6 to 12 months, adjusting your portfolio back to your original target allocation. In practical terms, this means selling some of the assets that have grown above their target percentage and buying more of the assets that have fallen below their target.

Yes, this means selling winners and buying underperformers. This feels counterintuitive. But it's actually disciplined, evidence-based investing, you're locking in gains from what performed well and buying more of what's currently undervalued at a relative discount.

Mark your calendar for a portfolio review every six months. Check your allocation percentages. If any asset class has drifted more than 5% from its target, rebalance. This habit alone significantly improves longterm portfolio performance and keeps your risk level where you intended it.

Age and Asset Allocation: The Shifting Formula

There's a traditional rule of thumb in investing called the "100 minus age" rule. It says: subtract your age from 100, and that number is the percentage of your portfolio that should be in stocks. The rest goes to bonds and safer assets.

So a 25yearold would hold 75% in stocks, 25% in bonds, and cash. A 45yearold would hold 55% in stocks, 45% in bonds, and cash.

This rule is a useful starting point, but it needs context for Nigerian investors. Because of the dual threat of naira devaluation and high inflation in Nigeria, most Nigerian financial advisors would argue for slightly higher equity and dollar asset exposure than the traditional formula suggests, because being too conservative in a high-inflation environment means your money's purchasing power erodes even while your nominal returns look decent.

A modified rule for Nigerian investors might look like this: younger investors (20s and early 30s) should lean heavily toward growth assets, 60–70% in stocks and dollar investments. Middle-aged investors (late 30s to mid40s) should have a more balanced split, 40–50% in growth assets, the rest in stable instruments. Investors closer to their goals or retirement should tilt heavily toward stability, 20–30% in growth assets, the majority in fixed income and cash.

As you age and your financial situation evolves, gradually shift your allocation from aggressive to conservative. This is called the glide path. Your portfolio slowly, deliberately becomes more protective as you approach the moment you'll need to use the money.

A Real Example: Building Tolu's Portfolio From Scratch

Let me bring all of this to life with a real Nigerian scenario.

Meet Tolu. She's 31. She works at a marketing agency in Abuja, earning ₦180,000/month. She has been reading Happyinvest articles for three months and is ready to build her first real, intentional portfolio. She can invest ₦35,000/month.

Tolu's financial goals:

Goal 1: Emergency fund (needs ₦250,000, about 3 months of expenses). Timeline: 8 months. Type: Conservative.

Goal 2: General wealth building for the next 15 years, she wants significant wealth by age 46. Timeline: 15 years. Type: Aggressive.

Goal 3: Down payment for land in her hometown in 4 years, target ₦1.5 million. Timeline: 4 years. Type: Conservative to moderate.

Tolu's allocation strategy:

Because she has three different goals with different timelines, she doesn't use a single portfolio; she uses separate buckets.

Bucket 1 Emergency fund (₦10,000/month): 100% money market fund on Cowrywise. No stocks, no risk. Just safe, liquid, growing at 20% p.a. while she builds the ₦250,000 target.

Bucket 2 Land savings (₦12,000/month): 60% Tbills and FGN savings bonds. 40% in a balanced mutual fund through Stanbic IBTC. Moderate but mostly safe, targeting growth toward ₦1.5 million in 4 years.

Bucket 3 Longterm wealth (₦13,000/month): 35% Nigerian stocks via a stockbroker (GTCO, MTN, BUA Foods). 35% US stocks and ETFs on Bamboo (mostly S&P 500 VOO). 20% equity mutual fund via ARM. 10% UPDC REIT. This is Tolu's wealth engine. She hasn't touched this for 15 years.

Within 8 months, Tolu's emergency fund is complete, and she redirects that ₦10,000/month into her long-term wealth bucket, supercharging her compounding.

This is what intentional, goal-based asset allocation looks like in practice. Not "I invest in whatever" but a clear, structured plan where every naira has an assigned purpose and a portfolio architecture matched to that purpose.

The Mistakes That Kill Good Allocations

Even investors who understand asset allocation make these errors. Be aware of them.

Overconcentrating in one asset because it's performing well. When Nigerian stocks are having a great year, the temptation is to shift everything there. When the NGX crashed, those investors suffered completely unnecessary losses. Stick to your allocation even when one asset looks irresistible.

Never rebalancing. Setting an allocation and forgetting it for 5 years means your portfolio has drifted far from where you intended. The risk profile you started with is no longer the risk profile you have. Rebalance consistently.

Having an allocation that doesn't match your real risk tolerance. Copying someone else's aggressive portfolio because it looks impressive, then panicking and selling when it drops 20%, that's worse than having a conservative portfolio you can actually stick to. Know yourself honestly.

Treating all your money as one portfolio. Your emergency fund, your vacation savings, and your retirement nest egg should not all be in the same investments. Different goals = different allocations = separate buckets.

Ignoring dollar exposure entirely. For Nigerian investors, having zero dollar-denominated assets is a significant risk. The naira's historical trajectory makes this one of the most important allocation decisions a Nigerian investor can make. Even 20–25% in dollar assets makes a meaningful difference to your longterm wealth preservation.

Chasing last year's top performer. The asset class that did best last year is often not the one that does best next year. Asset allocation is about balance across cycles, not chasing whatever is hot right now.

How to Start Building Your Allocation Today

You do not need a financial advisor or a complex spreadsheet to implement asset allocation. Here's a practical starting sequence.

First, write down your financial goals. For each goal, note the target amount, the timeline, and whether you can afford for that money to fluctuate in value. This gives you your basic framework.

Second, assess your risk tolerance honestly. If you've never experienced a portfolio drop before, lean toward the balanced model to start. You can always shift toward being more aggressive as you develop the emotional experience of riding market fluctuations.

Third, open the accounts you need. At minimum: a money market account (Cowrywise or ARM), a Nigerian stock brokerage account (Chaka, Trove, or a traditional broker), and a dollar investment account (Bamboo or Risevest). These three give you access to all the main asset classes.

Fourth, set up automatic monthly contributions to each account in proportions that match your chosen model portfolio. Make this automatic; remove willpower from the equation.

Fifth, set a calendar reminder every 6 months to review your allocation percentages and rebalance if any asset class has drifted more than 5% from its target.

Sixth, revisit your overall allocation strategy once per year. Ask: Have my goals changed? Has my timeline shifted? Has my income grown? Adjust accordingly.

That's the complete system. Not complicated. Not expensive. Not something that requires a finance degree. Just intentional, structured, consistently executed.

Final Word

Asset allocation is not a concept for rich investors with complex portfolios. It's the foundation that every investor at every level needs to build first. Because without it, you're not really investing. You're just spending money on financial products and hoping for the best.

With it, you have architecture. You have a plan where every naira has a purpose, every asset plays a role, and the whole portfolio works together in a way that is bigger, more resilient, and more powerful than any single investment could ever be.

You now understand what most Nigerian investors don't. You know the asset classes. You know how to choose your allocation based on your goals, timeline, and risk tolerance. You have three model portfolios to work from. You know what rebalancing is and why it matters.

The only thing left is to actually build your portfolio intentionally, deliberately, and starting today.

At Happyinvest, we make this simple enough for anyone to start. And you just proved that.

Making Money Simple. Building Wealth Daily.