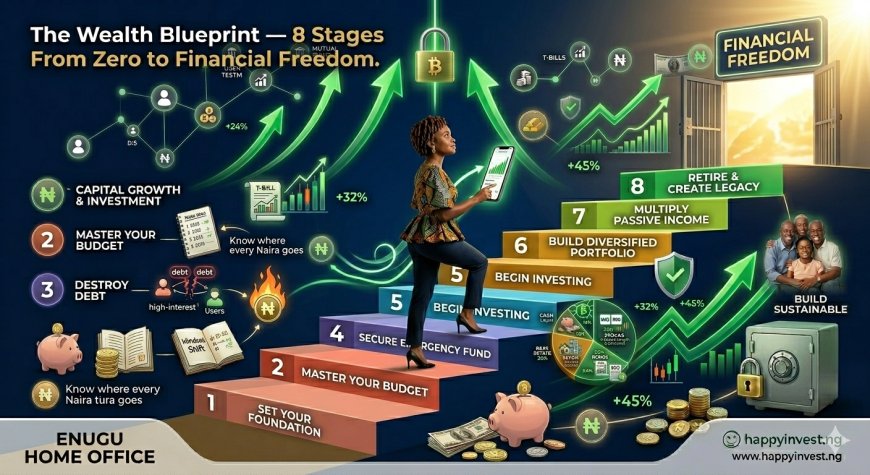

The Wealth Blueprint: How to Build Wealth From Zero

Ready to build real wealth from zero? Happyinvest's complete Wealth Blueprint breaks down 8 clear stages: mindset, income, budgeting, debt, emergency fund, investing, multiple income streams, and protection. With real ₦ examples and actionable steps for every Nigerian ready to stop wishing and start building. Your roadmap starts here.

Making Money Simple. Building Wealth Daily.

Let me start with a question that I want you to sit with for a moment.

If someone handed you ₦1 million right now, no strings attached, what would happen to it in the next 12 months?

Be completely honest.

Would it grow? Would it disappear into lifestyle, family obligations, and impulse spending? Would it sit in a savings account earning 4% while inflation quietly ate it alive?

If you're not sure of the answer or if you suspect the money would just... vanish, then today's article was written specifically for you.

Because here's the thing most people don't realize: the problem with building wealth in Nigeria is almost never the absence of money. It's the absence of a blueprint.

A blueprint is what separates someone who earns ₦80,000 a month and quietly builds ₦15 million over 10 years from someone who earns ₦300,000 a month and wonders where it all goes at the end of every month. One person is following a plan. The other is improvising. And in finances, improvising is expensive.

Today, I'm giving you the blueprint. Not a vague, feel-good motivation piece, but a real, stage-by-stage roadmap for building wealth from absolutely zero. From wherever you are right now. With whatever income you currently have.

This is going to be long. It's supposed to be. Save it. Read it in sections. Share it with your friends. Because this is the kind of article that, if you actually follow it, will look like a turning point when you look back on your life five years from now.

Are you ready? Let's build.

First, What Does "Building Wealth From Zero" Actually Mean?

Before we get into the roadmap, I need to give you a clear picture of what we're actually building toward because if the destination is vague, every road looks the same.

Building wealth from zero means starting from your current position, whatever that looks like, and deliberately, consistently moving toward a financial life where:

Your money works harder than you do. Your investments generate income even when you're sleeping. You have genuine financial options, the ability to say no to bad jobs, bad deals, and bad situations because you have a financial cushion. You're not anxious about money. And eventually, the income from your assets covers your expenses so that working becomes a choice, not a compulsion.

That's the destination. Not a number in a bank account is a state of financial freedom and security.

And here's what I need you to understand about that destination: it is absolutely available to ordinary Nigerians earning ordinary incomes. I'm not talking about Dangote-level wealth, I'm talking about the kind of financial freedom that thousands of quiet, disciplined Nigerians are building right now, on salaries that most people would consider unremarkable.

The secret isn't income. The secret is the blueprint. And the blueprint is what we're about to map out.

Stage 1: The Mindset Reset The Foundation Beneath the Foundation

Before you touch a single investment app, before you open a savings account, before you even write a budget, something more fundamental has to change.

Your relationship with money.

I know you've probably heard this before. "Mindset, mindset, mindset." It can start to sound like a cliché. But I want to go deeper than the cliché, because this isn't about positive thinking. This is about diagnosing and replacing specific beliefs that are actively sabotaging your financial decisions without you even knowing it.

Here's what I mean. Growing up in Nigeria, many of us absorbed financial beliefs that were never consciously chosen. Beliefs like:

"Money is hard to get and easy to lose." This belief makes you afraid to invest because investing feels like risking something precious and scarce. So you keep money in a savings account earning nothing, watching inflation quietly destroy its value, telling yourself you're being "careful."

"Rich people either got lucky or did something questionable." This belief makes wealth feel morally suspicious. It creates a subconscious resistance to building wealth because some part of you associates financial success with negative things. So you unconsciously self-sabotage. You sabotage savings with impulse spending. You walk away from good opportunities. You downplay your own financial ambitions.

"Investing is for people with a lot of money. I'll start when I earn more." This belief is perhaps the most expensive one of all. Because the people who wait until they "earn more" to start building good financial habits almost always find that more income just means bigger expenses. The habits don't change. The wealth doesn't come.

These beliefs need to be named, challenged, and replaced before anything else. Because you will build whatever your beliefs support. And if your beliefs say wealth is not for you, every action you take will unconsciously prove that belief right.

The mindset shifts you need to make:

Replace "I can't afford this" with "How can I afford this?" The first statement shuts down your thinking. The second one opens it to solutions. Ask the question. Let your brain work on it.

Replace "I'll start when I'm ready" with "I'll start and get ready as I go." You will never feel completely ready. The preparation comes from doing, not from waiting to do.

Replace "wealth is for lucky people" with "wealth is the predictable result of consistent right decisions over time." This is simply true. Study any wealthy person carefully, and you'll find a pattern of decisions, not a moment of luck, that built their financial life.

Replace "saving is sacrifice" with "saving is voting for my future self." Every naira you save instead of spending is a vote for the version of you that has options, freedom, and peace of mind. That's not punishment. That's the most loving thing you can do for yourself.

Your Stage 1 action: Write down three money beliefs you currently carry that might be limiting you. Then write the belief you want to replace each one with. Put that paper somewhere you see daily. This is the foundation before the foundation.

Stage 2: Income Clarity: Know What You Have and Maximize It

You cannot build wealth on income you haven't fully understood and optimized. So before we talk about what to do with your money, we need to talk about maximizing how much money you have to work with.

Two questions to start with.

First: Do you know your exact monthly take-home income?

Not approximately. Exactly. After every deduction, tax, pension, cooperative deductions, whatever comes out before it hits your account.

If you're employed, this number should be precise. If you're a business owner or freelancer, this number requires more work. Average your last 6 months of income to get a reliable figure.

You cannot build a wealth blueprint on a vague income number. Know your number.

Second: Is your income the highest it can realistically be right now?

Here's a hard truth: most Nigerians are underpaid relative to their skills, not because employers are necessarily evil, but because they haven't invested in making their skills more valuable, haven't negotiated, haven't looked for better opportunities, or haven't built any income outside their salary.

Your income is not fixed. It is a variable you have significant control over.

In 2026, there are several reliable levers for increasing your income relatively quickly:

Skill investment. The fastest legal way to increase your income is to make your skills more valuable. This could mean a relevant certification in your industry, learning a high-demand digital skill like data analysis, UI/UX design, copywriting, software development, or digital marketing, or developing deeper expertise in your current field that makes you genuinely harder to replace and easier to pay more.

Negotiation. Research shows that most people never ask for a raise, and most people who ask for one get at least something. If you've been in your current role for more than 12 months and your output has been strong, the conversation about compensation deserves to happen. Prepare for it with data: what the market pays for your role, what value you've added, and what you're asking for specifically.

A side hustle that matches your skills. What do you know how to do that someone else will pay for? Graphic design. Writing. Photography. Social media management. Baking. Tailoring. Financial consulting. Event planning. Virtual assistance. The list is genuinely endless. A side hustle adding even ₦20,000–₦40,000 a month dramatically accelerates your wealth blueprint.

Your Stage 2 action: Write down your exact monthly take-home. Identify one specific thing you can do in the next 90 days to increase your income by at least 10–15%. Not eventually. In the next 90 days. Make it concrete.

Stage 3: Budget and Control Give Every Naira a Destination

Now that you know what's coming in, it's time to decide intentionally where every single naira goes before the month starts, not after it ends.

Budgeting is not a restriction. Its direction. It's the difference between a ship with a captain and a ship adrift. Same ship, same ocean, completely different destination.

The framework I recommend for most Nigerians is the 50-30-20 rule:

50% of take-home income goes to Needs. Rent or housing. Food. Transport. Data and phone bills. Utilities. Children's school fees. These are the expenses your life cannot function without.

30% of take-home income goes to Wants. Outings and entertainment. Clothing beyond the basics. Subscriptions. Gifts and social events. Lifestyle upgrades. These matter for your quality of life, but they're things you could reduce if necessary.

20% of take-home income goes to Financial Goals. Savings. Investments. Debt repayment. Emergency fund building. This 20% is your future. It moves before your hands touch it.

Now, I know what some of you are thinking. "My rent alone takes 50% of my income. How does this work for me?"

Fair. Lagos is expensive. So adjust. Maybe it's 65-15-20. Maybe it's 70-10-20 for now. The exact percentages are less important than this non-negotiable principle: the 20% for financial goals is protected first, every single month, no matter what.

Everything else works around it.

The practical system that makes budgeting actually work:

Automate your savings transfer. The moment your salary hits, a fixed amount moves automatically to your savings or investment account. Before you pay for groceries. Before you settle any bill. Before your fingers consciously touch the money. This removes willpower from the equation, which is the entire point.

Track weekly, not monthly. Checking your spending once at the end of the month is like weighing yourself once a year; you discover problems too late to fix them. A quick 10-minute weekly check keeps you aware and in control throughout the month.

Identify your money leaks. For most Nigerians, there are 2–3 categories of spending that are significantly higher than they should be, and the person genuinely doesn't know because they've never tracked carefully. Food delivery, random transfers to acquaintances, impulse online shopping, and multiple streaming subscriptions. These leaks are costing you wealth silently every month. Find them. Plug them.

Your Stage 3 action: Write next month's budget before the month begins. Allocate your take-home across all three categories. Set up an automatic transfer for your 20% financial goals portion on your next salary day. Do it before anything else.

Stage 4: Debt Freedom Cut the Chains That Are Holding You Back

I want to talk about debt like a big brother who loves you enough to be direct.

If you're carrying high-interest consumer debt right now, BNPL balances from Palmpay, Carbon, or FairMoney, personal loans at 5–10% monthly interest, borrowed money from people you keep avoiding, every naira you invest while carrying that debt is working against itself.

Here's the math: if you're paying 10% monthly interest on a ₦50,000 loan, that's ₦5,000 per month in interest alone. Per year, you're paying ₦60,000 in interest on ₦50,000 borrowed. That's a 120% annual cost of debt.

Can your investments earn 120% annually to offset that? No legitimate investment can. Which means carrying that debt while investing is a guaranteed losing proposition. The debt must go first.

The snowball method is your debt elimination weapon:

List every bad debt you have. From the smallest outstanding balance to the largest. Don't order by interest rate; order by balance size. This is important.

Pay the minimum on every debt except the smallest one.

Throw every extra naira you can find into side hustle income, expense reductions, and any windfalls at the smallest debt until it's gone.

When the smallest debt is cleared, take all the money you were paying on it and add it to the payment on the next debt.

Repeat. The momentum builds as each debt falls. By the time you're attacking the larger debts, you have a formidable payment amount focused on each one.

Why the snowball method instead of attacking the highest-interest first? Because debt elimination is as much a psychological battle as a financial one. Quick wins on small debts create momentum, confidence, and motivation that keep you going. The math might slightly favor the highest-interest approach, but the psychology overwhelmingly favors the snowball.

What about good debt? A mortgage on appreciating property, a low-interest business loan generating revenue, and a student loan that multiplies your earning capacity don't fall in the same category. We're specifically targeting consumer debt: borrowing to spend rather than to build.

Your Stage 4 action: Write down every consumer debt you have, smallest to largest. Make your first snowball payment this month. Commit to not taking on any new consumer debt while this process is running.

Stage 5: Build Your Emergency Shield Protection Before Growth

You've reset your mindset. You've optimized income. You're budgeting intentionally. You've eliminated bad debt or have a plan running. Now, before you invest a single naira in anything other than the safest possible option, you need to build your emergency fund.

This is the step most people skip in their excitement to start investing. And then they invest, something goes wrong in life, they're forced to withdraw from their investments at the worst possible time, they see a loss, and they conclude that investing doesn't work.

It works. They just didn't have a shield.

What is an emergency fund? It's 3 to 6 months of your total monthly expenses, sitting in a liquid, interest-earning account that you touch only for genuine emergencies. Medical crisis. Job loss. Essential equipment breakdown. Genuine family emergency. Not holidays. Not new phones. Not "I want something."

Where to keep it: A money market fund on Cowrywise, ARM Investment Managers, or Stanbic IBTC. Here's why this is better than a regular savings account: your money earns 18–22% per annum instead of 4–6%. It remains fully liquid and accessible within 24–72 hours when you need it. It's regulated and safe. Your emergency fund is not sitting idle while it protects you. It's growing while it protects you.

How to build it: Calculate your monthly expenses honestly. Multiply by 3 for your minimum target. If you spend ₦80,000/month, your target is ₦240,000. On a savings rate of ₦15,000/month dedicated to this fund, you hit your target in 16 months. Yes, it takes time. That's fine. Start and stay consistent.

What the emergency fund actually buys you: Peace of mind. And more than that, it buys your investments time. When an emergency comes (and it will come), you handle it from your shield fund without touching your investments. Your investments stay invested. Compound interest keeps running. Your wealth-building doesn't restart from zero because of one bad month.

Your Stage 5 action: Open a dedicated money market fund account today specifically for your emergency fund. Name it "Emergency Shield" so you're psychologically reminded of its purpose every time you see it. Calculate your 3-month target. Set up your monthly contribution.

Stage 6: Invest and Let Compound Interest Do the Heavy Lifting

We're here. The stage most people want to start with, but only now, after building the foundation, are you truly ready for.

Investing is how your money stops working just for you and starts working with you. Every naira you invest is a tiny employee that works 24 hours a day, 365 days a year, never calls in sick, never asks for a raise, and if you leave it alone long enough, eventually earns more than you do.

But here's the thing that separates wealth builders from people who dabble in investing: it's not about picking the perfect stock or finding the hottest opportunity. It's about consistency, time, and letting compound interest do what it does.

Let me show you why with real numbers.

If you invest ₦10,000 every month starting today at an average annual return of 20%, which is achievable with a diversified Nigerian and dollar portfolio, here is what happens:

After 5 years: approximately ₦960,000. You contributed ₦600,000. Your investments made you ₦360,000 without any additional work from you.

After 10 years: approximately ₦7.7 million. You contributed ₦1.2 million. Compound interest added over ₦6.5 million.

After 20 years: approximately ₦77 million. You contributed ₦2.4 million. Compound interest added ₦74.6 million.

That's not a typo. ₦10,000 a month, consistently invested, produces ₦77 million in 20 years. The compound interest contributes 30 times what you personally put in. This is why wealthy people always say time in the market beats timing the market. Start early. Stay in. Let it compound.

The investment ladder for Nigerians building from zero:

Rung 1 Money Market Funds. This is where you start. Safe, liquid, currently earning 18–22% per annum in Nigeria. Available on Cowrywise, ARM, Stanbic IBTC from ₦1,000. Once your emergency fund is complete, your money market fund continues growing and becomes a pillar of your broader portfolio.

Rung 2 Nigerian Stocks. Once you've built some knowledge and your emergency fund is solid, add quality Nigerian equities. GTCO, Zenith Bank, MTN Nigeria, BUA Foods, Dangote Cement. Buy companies with strong earnings, consistent dividends, and proven management. Hold for the long term. Platforms like Chaka, Trove, and traditional NGX brokers give you access.

Rung 3 Dollar Investments. Add US stocks and ETFs through Bamboo, Risevest, or Trove. Start with a simple S&P 500 ETF like VOO, which gives you ownership in Apple, Microsoft, Amazon, Google, and 496 other companies in one purchase. This protects your wealth from naira devaluation while giving you access to global market growth. Start with as little as $5.

Rung 4 REITs and Real Estate Exposure. UPDC REIT on the NGX gives you real estate exposure from a few thousand naira. As your portfolio grows, consider physical property land in developing areas or residential property in high-demand locations.

The investing non-negotiables:

Invest in payday before you spend anything else. Automate it.

Never stop contributing just because the market is down. Dips mean you're buying at a discount. The investors who kept contributing through Nigeria's market downturns are the ones who benefited most from the recovery.

Diversify from day one. Nigerian stocks, dollar assets, fixed income. Don't concentrate everything in one place.

Check your portfolio quarterly. Not daily. Daily checking breeds emotional decision-making. Quarterly checking breeds strategic thinking.

Never invest money you'll need within 12 months. That money belongs in a money market fund or T-bill, not in stocks.

Your Stage 6 action: Open one investment account this week if you don't have one. Start with a money market fund if you're a complete beginner. Transfer whatever you can. ₦5,000 is enough to begin. The habit of investing is more valuable than the amount you start with.

Stage 7: Multiply Your Income, Build Streams That Work Without You

There's a ceiling to how much wealth you can build with one income stream, no matter how well you invest. The ceiling is simply the gap between what you earn from one source and what you spend. The bigger the gap, the more you invest. But with one source, the gap has a natural limit.

Multiple income streams break that ceiling.

This is not about burning yourself out with five different jobs. It's about strategically building income sources that, over time, require less and less of your active time to maintain. The goal is to move from trading time for money to building systems that generate money with decreasing time input.

The three levels of multiple income:

Level 1: Active secondary income. This requires your time and skill but outside your primary job. Freelancing your professional skills. Tutoring students. Managing social media for small businesses. Graphic design gigs. Photography. Running a small retail or food business. This level multiplies your income immediately but still requires your time.

Level 2: Scalable income. You create something once and it generates revenue repeatedly. An online course teaching a skill you have. An ebook or digital guide. A YouTube channel that earns ad revenue. A newsletter or blog that attracts sponsorships. A template pack or digital product. The income from these doesn't require you to show up to each transaction the way active income does.

Level 3 Passive investment income. Dividends from quality stocks. Interest from bonds and money market funds. REITs distributing rental income quarterly. As your portfolio grows, this level grows with it money generating money without any active work from you.

Most Nigerians building wealth from zero start at Level 1, build toward Level 2, and gradually watch Level 3 grow through consistent investing. This is not a quick process. It's a deliberate, multi-year construction. But every stream you add multiplies your wealth-building capacity.

Practical income streams available to Nigerians in 2026:

If you have professional skills, such as consulting, writing, design, engineering, or accounting, those skills have a freelance market. Platforms like Fiverr, Upwork, and local Nigerian networks are full of businesses that need exactly what you know.

If you're good at a craft or trade, such as baking, catering, tailoring, woodworking, or interior decoration, there's a market for premium, quality work. Don't compete on price. Compete on quality and positioning.

If you're knowledgeable about a subject students need help with, such as WAEC, JAMB, university courses, or professional exams, tutoring is an immediately accessible income stream that requires nothing except your time and knowledge.

If you have an audience, even a small, engaged one on any platform, that audience can be monetized through affiliate marketing, brand partnerships, digital products, or subscription content.

If you have investment capital, even modest amounts, dividend-paying stocks and money market funds can begin generating passive income immediately.

Your Stage 7 action: Identify one income stream you could realistically add in the next 60 days. Not five. One. Make a list of five potential clients, customers, or platforms you could approach. Reach out to the first one this week.

Stage 8: Protect and Scale Guard the Fortress You're Building

There is a specific kind of devastation that comes from watching years of careful wealth-building get destroyed in weeks by something that good planning could have prevented.

I'm talking about the person who spent 8 years building a portfolio, and then a serious illness wiped it all out in medical bills because there was no health insurance. Or the family that lost their home and savings in a fire because there was no property insurance. Or the children left fighting over an estate for years because their parent died without a will.

Wealth building without wealth protection is building a magnificent house without walls. Everything you've built is perpetually exposed to being destroyed.

Protection has four pillars for every Nigerian wealth builder:

Health Insurance. This is the most urgent. A serious medical event in Nigeria can cost ₦500,000 to several million naira. If you don't have health insurance, that cost comes directly from your savings, your investments, or your debt capacity. Individual health plans from Hygeia, AXA Mansard, Reliance HMO, or Leadway Assurance start from ₦15,000–₦50,000 per year. That's ₦1,250 to ₦4,200 per month. It costs less than most Nigerians spend on data subscriptions. Get it.

Life Insurance. If you have dependent children, a spouse, or parents who rely on your income, your death without life insurance is a financial catastrophe for them. Term life insurance provides a death benefit that protects your family's financial future if you die during the policy period. Providers like AIICO, ARM Life, FBN Insurance, and AXA Mansard offer accessible term policies. The younger and healthier you are when you buy, the cheaper the premium.

A Will. This is the one almost every Nigerian delays and it costs families enormously when people die without one. Dying intestate in Nigeria means your assets are subject to legal processes that can freeze estates for years and create family conflicts that destroy wealth and relationships. A licensed Nigerian lawyer can draft a basic will for a few thousand naira. If you own a bank account, investments, property, or a business, you need a will. Schedule this.

Portfolio Protection. As your investment portfolio grows, protect it through diversification; never concentrate more than 20–25% in any single asset. Rebalance annually to maintain your target allocation. Increase your contributions every time your income increases rather than just increasing your lifestyle.

Scaling: Protection without scaling is just preservation. As your wealth grows, you need to think about how to grow it faster and larger. This means seeking professional financial advice from a licensed CFP. It means looking at real estate as a wealth storage and growth vehicle. It means thinking about business equity building or investing in businesses that compound in value. It means thinking about generational wealth, what you're building that outlasts you and serves your children.

Your Stage 8 action: This week, get a quote for health insurance. This one action, if you don't currently have coverage, could save your entire wealth blueprint from being undone by one medical emergency.

The Blueprint Rule: The One Sentence That Summarizes Everything

After eight stages, dozens of strategies, and thousands of words, the entire wealth blueprint can be condensed into one sentence.

Earn more. Spend less than you earn. Invest the difference consistently. Protect what you build. Repeat for decades.

That's it. That's the whole thing.

Everything else, the budgeting frameworks, the investment platforms, the income stream strategies, the insurance products, is just the detail work that implements that one sentence in real, practical, Nigerian life.

The sentence is simple. The execution is where most people stumble. Not because it's complicated, it's genuinely not. But because it requires consistency over convenience. Discipline over impulse. Long-term thinking over short-term comfort.

The people who follow the blueprint don't have superpowers. They're not genius investors who pick the perfect stocks. They're not people who got lucky with one big break. They're people who decided at some point, often just like the moment you're in right now, that they were going to take their financial lives seriously. That they were going to follow a plan. That they were going to be consistent even when it wasn't exciting.

And they kept showing up. Month after month. Year after year. Quietly, steadily, building.

What Does Your Wealth Blueprint Look Like Right Now?

Here's what I want you to do before you close this article.

Look at the eight stages again. Honestly identify which stage you're currently in. Not where you wish you were. Where you actually are.

If you're at Stage 1, that's the starting line. Not a setback. The starting line. The only thing that matters from the starting line is that you take a step. Any forward step.

If you're at Stage 4, you have foundational work running and debt is the current mountain. Stay in the snowball. Don't skip to investing yet. Clear the chains first.

If you're at Stage 6, you're building. Now the work is consistency, patience, and not destroying your portfolio with emotional decisions.

If you're at Stage 7 or 8, you're in the scaling phase. The most important thing now is protecting what you've built and systematically adding to it.

Wherever you are, you are not behind. You are exactly where the choices you've made so far have brought you. And starting today, you get to choose differently.

The blueprint is in your hands. The question is what you do with it.

One Final Thing

Wealth is not a destination you arrive at. It's a direction you commit to.

It doesn't announce itself. It doesn't come with a trumpet and a celebration. It comes quietly, after years of decisions nobody saw and sacrifices nobody witnessed. And one day you look at your portfolio, your income streams, your financial security, and you realize that the person who made that decision to start, to follow the blueprint, to stay consistent, that person changed everything.

That person is you. Starting today.

At Happyinvest, we're here for every stage of this journey.

Making Money Simple. Building Wealth Daily.