How to Build a Financial Life Blueprint That Actually Works in 2026

Discover how to design a financial life blueprint. Learn how to manage money, invest, and build wealth with a structured plan.

A Financial Life Blueprint is not a budget. It is a complete, integrated map of where you are financially, where you are going, how you will get there, and what will protect you along the way. This is how you build one from scratch, for life.

- What a Financial Life Blueprint actually is and what it is not

- The six pillars every Blueprint must cover

- Step 1 — Take your financial snapshot (your starting coordinates)

- Step 2 — Define your financial vision and life goals

- Step 3 — Design your income architecture

- Step 4 — Master your cash flow and money zones

- Step 5 — Build your protection layer

- Step 6 — Create your investment and wealth-building plan

- Step 7 — Plan your legacy

- Step 8 — Install your review and accountability system

- Your personal Blueprint worksheet.

What a Financial Life Blueprint Actually Is and What It Is Not

Most people confuse a budget with a financial plan. A budget is a monthly spending document. It tells you what happened to your money last month and how much you are allowed to spend next month. It is useful, but it is not a blueprint. A blueprint is an architect's complete drawing of an entire building before a single brick is laid. It shows the structure, the systems, the load-bearing walls, the exits, and how everything connects.

A Financial Life Blueprint is the same concept applied to your financial existence. It is a living document that simultaneously captures your present financial reality, articulates your future financial destination, and maps the specific decisions, systems, and behaviours that will take you from one to the other across every dimension of your financial life, including income, spending, protection, investment, debt, taxes, and legacy.

Unlike a budget, which most people abandon within 90 days, a Financial Life Blueprint is designed to be revisited, not to be perfect. It is a north star, not a cage. It answers the four questions that most Nigerians have never formally answered about their own money:

Where exactly am I financially right now? Where specifically do I want to be, and by when? What is my precise plan for getting there? What will protect me if something goes wrong along the way?

The missing piece in most financial advice: Most financial content tells you what to do, save, invest, and budget. A Financial Life Blueprint tells you how everything connects. Saving for what? Investing for when? Budgeting toward which life? The blueprint provides the context that makes every individual financial decision coherent and intentional.

"If you don't have a plan for your money, your money will plan your life for you." CreditDirect Nigeria, Financial Independence Guide (2025)

The Six Pillars Every Blueprint Must Cover

A Financial Life Blueprint that omits any of these six pillars is incomplete, like a house without a roof or without foundations. Each pillar is interconnected. Weakness in one undermines all the others.

Step 1 — Take Your Financial Snapshot

Every blueprint begins with an honest assessment of exactly where you stand. Not where you think you stand. Not where you told someone at dinner you stand. Where you actually stand, in naira and kobo, right now. This is your financial starting coordinate — and without it, everything that follows is navigation without a map.

Calculate your net worth

Your net worth is the single most important number in your financial life. It is simply everything you own minus everything you owe. It is not your salary. It is not your job title. It is the true measure of your financial position at any moment in time.

Net Worth = Total Assets − Total Liabilities. If the result is positive, you own more than you owe. If it is negative, your liabilities exceed your assets, which is common in the early stages of life, and is not a crisis. It is a starting point. Write this number down, undisguised. It is the first honest line of your blueprint.

Map your monthly cash flow

For one complete month, track every naira of income and every naira of expenditure. Use your bank statements, not your memory. Most people who do this exercise for the first time are genuinely shocked by what they discover: the money spent on data and subscriptions, the food deliveries that add up, the informal social obligations, and the money that leaves the account without a clear destination. The purpose of this exercise is not to shame yourself. It is to see clearly. You cannot improve what you cannot measure.

Nigerian context: When tracking your cash flow, include mobile money transfers, POS transactions, cash withdrawals, family financial obligations (aso-ebi, family contributions, helping relatives), tithes and offerings, and any informal savings groups (ajo/esusu). These categories are often invisible in standard budgeting advice but represent significant financial flows for most Nigerian adults.

Step 2 — Define Your Financial Vision and Life Goals

Most people live financially reactive lives responding to bills, to needs, to social pressure, to what the month demands. A Financial Life Blueprint demands something different: a deliberate, written declaration of what you want your financial life to produce, and by when.

Your financial vision is not about a specific number. It is about the life that the number enables. Start by asking: What does financial freedom specifically mean for me in this life? Not what it means in a generic motivational post. For you. Does it mean never worrying about school fees? Does it mean leaving a full-time job by 45 to pursue something you love? Does it mean owning a home in a specific area, funding a parent's retirement, or leaving your children debt-free?

Immediate financial milestones

Emergency fund at target level. Specific high-interest debt eliminated. A defined savings account for a specific near-term purchase (laptop, travel, course). Your first investment account has been opened and funded. These are the goals that build the habit of execution and prove to yourself that your blueprint is real.

Life-stage milestones

Home ownership or a deposit saved. The marriage fund is fully planned. First investment portfolio at a specific value. Side income stream generating a target monthly amount. A skill or qualification acquired that increases earning capacity. Car purchased without debt. These goals anchor your blueprint to the life you are building right now.

Financial independence and legacy milestones

An investment portfolio generating passive income equal to your living expenses. Children's education is fully funded. Retirement provision in place. A Will written and updated. A family financial legacy is not just money, but values, knowledge, and structures that outlast you. These are the goals that give the entire blueprint its deepest purpose.

Goal-setting rule: Every financial goal in your blueprint must be SMART: Specific (exactly what), Measurable (exactly how much), Achievable (realistic given your income), Relevant (connected to your actual life vision), and Time-bound (a clear deadline). "Save more money" is not a goal. "Save ₦500,000 in a money market fund by December 2026 for a laptop and home office setup" is a goal.

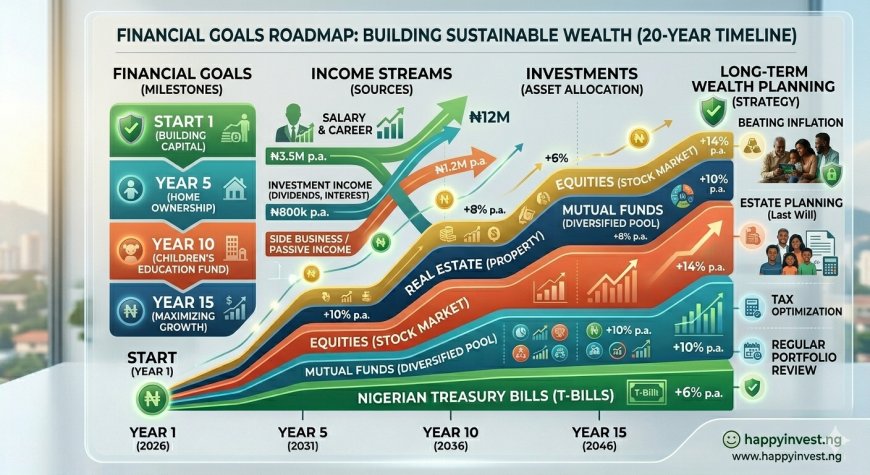

Step 3 — Design Your Income Architecture

Your income is the engine of your financial life. Everything else in your blueprint, your savings, your investments, your protection, is constrained or enabled by how much comes in and from how many sources. Most Nigerians have a single income source: their salary. This is not just a missed opportunity in Nigeria's volatile economy; a single income stream is a financial vulnerability.

Your blueprint should map your income across three layers, building from the foundation upward:

Layer 1 — Active Primary Income (your salary or main business income)

This is where most people start and where most people stay. Your blueprint should not just record this income but project it. Where do you realistically expect your primary income to be in 3 years? In 5? What specific actions, skills upgraded, certifications earned, promotions pursued, and business growth will drive that growth? A blueprint that assumes static income across 20 years is a plan for static wealth. Map the growth trajectory explicitly.

Layer 2 — Active Secondary Income (deliberate additional earned income)

Side hustles, freelance income, consulting fees, professional services, and teaching skills. Nigeria's gig economy has grown 43% since 2023. Digital marketing, UI/UX design, content management, data analysis, and virtual assistance now offer Nigerian professionals ₦80,000–₦400,000 monthly in additional income. Your blueprint should identify one specific skill-based income stream to develop, with a timeline and income target. This layer does not require a business it requires a monetisable skill applied deliberately.

Layer 3 — Passive and Portfolio Income (money working without your time)

Dividend income from NGX stocks, interest from bonds and money market funds, rental income from property, royalties, and business distributions. This is the ultimate income destination money that arrives whether you work that day or not. Building this layer takes years of consistent investment accumulation (Layers 1 and 2 fund this layer). Your blueprint should track the growth of passive income as a percentage of your monthly expenses. When it reaches 100%, you have achieved financial independence.

Step 4 — Master Your Cash Flow and Money Zones

A Financial Life Blueprint without a cash flow system is a vision statement without an engine. Once you know how much is coming in, you need a pre-decided, automatic system for allocating it the moment it arrives. The money zones framework below replaces the traditional budget with something more structural and psychologically sustainable.

Nigerian adjustment: Standard global frameworks suggest 50/30/20. For urban Nigerians dealing with high living costs in Lagos, Abuja, and Port Harcourt, where rent alone can consume 40% of income, a modified 60/15/15/10 split may be more realistic as a starting point. What matters is the direction of travel: over time, deliberately move toward the 50/10/25/15 target by growing income faster than lifestyle costs.

The automation imperative

The single most powerful mechanical feature of a Financial Life Blueprint is automation. Young professionals who maintain automated savings consistently save 31% more than those who manage transfers manually. On payday, your bank should execute standing orders that move money to designated accounts before you have the opportunity to spend it. Protection funds, investment contributions, and emergency savings should all be scheduled, not discretionary. The willpower required to "remember to invest" every month is a resource that depletes. Automation is the system that replaces willpower with infrastructure.

Step 5 — Build Your Protection Layer

Wealth building and wealth protection are not separate activities. They are simultaneous obligations. The most disciplined investment plan in the world can be destroyed by a single uninsured medical crisis, an unexpected income loss, or a liability lawsuit. Your blueprint's protection layer is the immune system of your financial life.

Step 6 — Create Your Investment and Wealth-Building Plan

Your investment plan is the section of your blueprint that translates the surplus created by your income architecture and cash flow system into compounding wealth over time. It is not a list of hot stocks. It is a structured, systematic approach to deploying capital across asset classes that align with your goals, risk tolerance, and time horizon.

Match assets to timelines

Short-term goals (0–2 years) should be funded with stable, liquid instruments — money market funds and short-dated treasury bills. You need this money soon; you cannot afford to see it drop 30% in a market correction. Medium-term goals (2–7 years) suit balanced funds, fixed income instruments, and moderate equity exposure. Long-term goals (7+ years) retirement, generational wealth, and financial independence are where equity funds, NGX stocks, ETFs, and compounding can do their most extraordinary work. Time is the engine of compound returns; mismatching your assets to your timelines is one of the most costly investment mistakes.

The core investment portfolio for a Nigerian

Your blueprint's investment section should specify, in writing, the exact allocation of your investment capital across instrument categories. A robust Nigerian portfolio typically includes a stability layer (money market funds and T-bills), an income layer (FGN bonds and dividend stocks), a growth layer (equity mutual funds and NGX ETFs), and an FX hedge layer (dollar funds and international ETFs). The specific percentages should reflect your age, income stability, and goal timelines, not your enthusiasm for any particular asset class at any particular moment.

The reinvestment discipline

Your blueprint should contain an explicit, written policy on what happens to every dividend payment, bond coupon, and investment distribution received. In the wealth-building years (typically the first decade of disciplined investing), the answer should be automatic: reinvest everything. The compounding arithmetic is unambiguous; money taken out early halts its compounding permanently. Every naira of returns that re-enters the portfolio has decades to multiply.

Step 7 — Plan Your Legacy

A Financial Life Blueprint that ends with your last investment statement is a blueprint for personal enrichment — admirable, but incomplete. A truly comprehensive blueprint includes explicit planning for what happens to the wealth you build when you are no longer alive to manage it.

Write your Will — now, not someday

Seven in ten Nigerians die without a valid Will. When that happens, the state and customary law do not decide who receives everything you spent a lifetime building. A Will is a legally binding document that gives your wishes the force of law. It appoints executors, names beneficiaries, designates guardians for minor children, and can exclude individuals who would otherwise inherit under default customary rules. It costs between ₦50,000 and ₦300,000 with a qualified Nigerian lawyer. It is the single highest-return legal investment an adult Nigerian can make.

Pension and RSA management

Your Retirement Savings Account is often your largest single financial asset and yet the least attended to by most Nigerian workers. Your blueprint should include a review of your RSA balance, your Pension Fund Administrator's performance, and whether your current contribution level (employee plus employer combined) is sufficient to fund your desired retirement lifestyle. For most Nigerians, it is not, and voluntary additional contributions should be planned explicitly.

Financial knowledge transfer

Legacy is not only about transferring assets. It is about transferring knowledge. A Financial Life Blueprint includes a plan for ensuring that the people who inherit your wealth also understand how to steward it. Teaching your children the principles in this blueprint. Having frank conversations with your spouse about investment accounts and where everything is. Leaving a financial instruction letter alongside your Will detailing every account, platform, and policy, with clear guidance for your executor. These acts of financial transparency are as important as the assets themselves.

Step 8 — Install Your Review and Accountability System

A Financial Life Blueprint written once and never revisited is a historical document. A Financial Life Blueprint reviewed regularly is a living management system. The difference between the two is the difference between financial drift and financial direction.

Your Personal Blueprint Worksheet

Use the prompts below to begin writing your own Financial Life Blueprint. Complete each section honestly. This document is for you; it has no audience, no judgment, and no requirement to be impressive. It only requires that it be true.

Your Blueprint Is a Living Document — Not a Finished One

The most important thing about your Financial Life Blueprint is not that it be perfect on the day you write it. It is that you write it. And then you return to it. The blueprint you write today will look different from the one you have in 5 years because you will have grown, your income will have changed, your goals will have evolved, and your understanding of money will be deeper and more nuanced.

Financial clarity is not a destination. It is a practice. The people who build lasting financial lives are not those who make the single best investment decision. They are the ones who build the system, review it honestly, adjust it thoughtfully, and never stop asking: Does my financial life as I am currently living it reflect the financial life I am intentionally designing?

Your blueprint is your answer to that question, written down, made specific, reviewed regularly, and updated as life demands. Nothing about your financial future is fixed. But nothing about it will improve either, without a deliberate plan for the direction it should travel.

Your action today: Open a new document or notebook. Write "MY FINANCIAL LIFE BLUEPRINT" at the top. Complete Section A of the worksheet above, just your current financial snapshot. That single act of financial honesty is the first brick of the structure you are building.

Get the PDF below as a gift

This article is for educational and informational purposes only. It does not constitute personalized financial, legal, or investment advice. For advice tailored to your specific circumstances, please consult a qualified financial planner or licensed financial advisor.